Reply To:

Name - Reply Comment

Moody’s Investors Service yesterday said Sri Lanka’s external reserves remain still low even after taking receipts of inflows of around a billion dollars in the last couple of weeks, which helped the country to recoup part of the lost assets caused by the settlement of a billion dollar sovereign bond and other liabilities through August.

In an update to the Sri Lankan sovereign issued yesterday, Moody’s continued to hold the view of “ rising risk of debt default,” for the country, a concern which grew in intensity since of late given the limited refinancing options for the country amid hefty foreign debt obligations and pandemic related stress on non-debt creating foreign inflows such as tourism, direct investments and exports to a certain degree.

“Without sizeable external financing that is relatively secure and long-term, we expect foreign exchange reserves to continue declining over the next two to three years,” the rating agency said.

Moody’s in July placed Sri Lanka’s sovereign rating at Caa1 under review for downgrade citing heightened risk of default, just days ahead of the country settling a billion dollar sovereign bond amid dwindling reserves.

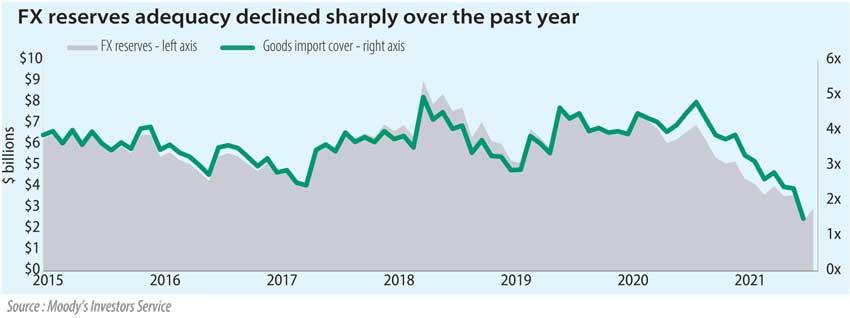

Post the bond settlement, Sri Lanka’s foreign reserves plunged to post-war low US$ 2.8 billion, equivalent for 1.8 months of imports before recouping to US$ 3.6 billion in August after the country took receipt of US$ 787 million from the International Monetary Fund’s Special Drawing Rights allocation and US$ 150 million from the Bangladesh Bank as part of a US$ 250 million swap arrangement.

Further Sri Lanka also has a US$ 1.5 billion worth Renminbi currency swap with China on stand-by and a further US$ 300 million from the China Development Bank awaiting disbursement.

Besides, Sri Lanka also plans to divest some State-owned assets to generate foreign inflows and recently called for a new foreign currency term financing facility from banks, putting into use the multiple tools in its armoury to shore up reserves.

However, Moody’s, which estimated the August reserves at nearly US$ 3.0 billion as their definition of reserves excludes, “gold and special drawing rights,” showed they remain, “43 percent lower than at the beginning of the year and around US$ 600 million lower compared to the end of June”.

But Moody’s measures Sri Lanka’s foreign debt maturities at around US$ 4 - 5 billion annually through at least 2025.

Given the size of the foreign debt coming up due annually, the rating agency isn’t convinced if the country could ride through the near to medium term external liquidity pressures with stop-gap measures currently been employed by the government along with the Central Bank.

“However, such inflows are piecemeal and boost FX reserves only temporarily and marginally given the government’s external repayment schedule,” Moody’s said.

While the temporary restrictions on outflows on select imports and outbound remittances help to retain some foreign resources in the country while being effective in the short term, such measures, “could weigh on economic activity and deter investment inflows”, they added.

While the pandemic has weighed on direct inflows and delayed the recovery of tourism inflows, the rating agency expected foreign direct investments to average US$ 1.0 billion in 2021-22 considering the development of Colombo Port City and the exploration of other avenues.

Moody’s also expressed hope that the current vaccination drive would help the country to re-open the economy and its borders to provide a boost to the tourism sector and other non-debt generating inflows from 2022 onwards.