Reply To:

Name - Reply Comment

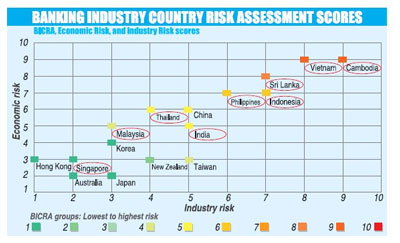

While observing the economic imbalances building up in Sri Lanka with the pickup in growth in private sector credit, a global rating agency, Standard & Poor’s Rating Services (S&P) identified the country’s banking sector as having a very high risk in the South and South East Asian region, slightly better than only Vietnam and Cambodia.

While observing the economic imbalances building up in Sri Lanka with the pickup in growth in private sector credit, a global rating agency, Standard & Poor’s Rating Services (S&P) identified the country’s banking sector as having a very high risk in the South and South East Asian region, slightly better than only Vietnam and Cambodia.

In a Banking Industry Country Risk Assessment (BICRA) matrix which maps out each banking system with a score ranging from low risk (1) to very high risk (10), S&P has assigned Sri Lanka with a score of ‘8’, indicating the very high economic and industry risk to the Sri Lankan banks.

“Sri Lanka went through a 28 percent credit growth for two consecutive years. That is rapid by any stretch of i magination,” said the Managing Director and Lead Analytical Manager, Financial Services Ratings at S&P, Ritesh Maheshwari.

While maintaining that credit growth is the key risk faced by the Sri Lankan financial system, he said even though the loan growth was reduced to about 20 percent, it still remained higher than nominal GDP growth.

While maintaining that credit growth is the key risk faced by the Sri Lankan financial system, he said even though the loan growth was reduced to about 20 percent, it still remained higher than nominal GDP growth.

“And it is slowing down now, which means a correction is happening before it become an unsustainable bubble. If this moderate credit growth continues for a year or two, we will be getting to a phase where we can gradually start to raise the credit and increase the penetration from the current 35 percent (Credit to GDP), and still be on a very stable growth path for the economy”.

“Any faster we are definitely taking risks,” he noted.

Credit to GDP ratio in Sri Lanka has been rising rapidly, now at 34 percent, but still one of the lowest in Asia-Pacific.

In 2011 and 2012, the private sector credit grew by 34 percent and 23 percent respectively, due to the post-war euphoria. This high exposure of banks’ balance sheets has led to some deterioration in the Non-Performing Loan (NPL) ratio of the Sri Lankan banks.

“We view this credit growth as high in the context of a relatively low income economy and low initial leverage. NPLs may also rise in other segments as the operating environment remains challenging and the loan book seasons,” Maheshwari added.

However, he said the banking sector profits are sufficient to absorb any risks arising from pawning or other loan book exposures.

Explaining why high credit growth is perceived as very high risk by the rating firm, he said when too much credit was available, the system would not have the ability to allocate those credit efficiently for those sectors which credit was actually needed.

Apart from that he said, too much credit would also not be efficiently utilized.

“And, the moment anything is freely available in abundance, it ends up going to the wrong place. It could also end up going to the sectors or persons who already have credit over leveraging them beyond capacity and that ends up in hurting,” he quipped. (DK)