If those who received vehicle permits for economic development still had those vehicles, it could be said that they contributed to economic growth. However, these permits are often sold within a year, which is problematic. The Minister’s actions are infringing upon the basic rights of the citizens and violate the constitution

If those who received vehicle permits for economic development still had those vehicles, it could be said that they contributed to economic growth. However, these permits are often sold within a year, which is problematic. The Minister’s actions are infringing upon the basic rights of the citizens and violate the constitutionReply To:

Name - Reply Comment

It has been revealed that duty-free vehicle permits are being issued by misinterpreting a clause in the Excise Act which supports tax free importing of vehicles for economic development purposes

|

Motor Vehicle Permits on Concessionary Terms continue to be granted certain groups of individuals disregarding the provisions of the Excise Act Duty-free vehicles have been granted to government officials both during their service and upon their retirement Since the 1990s, politicians, government officials, and dignitaries have denied the country substantial tax revenue by exploiting this clause and importing vehicles |

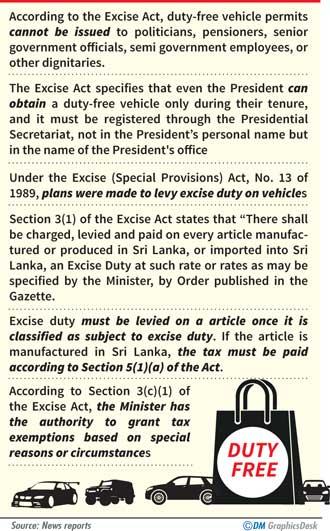

According to the Excise Act, duty-free vehicle permits cannot be issued to politicians, pensioners, senior government officials, semi government employees, or other dignitaries. The Excise Act doesn’t authorise the issuance of vehicle permits to people serving in such capacities. However, Motor Vehicle Permits on Concessionary Terms continue to be granted to these groups, disregarding the provisions of the Excise Act. During an investigation done by this newspaper it was revealed that these permits are being issued by misinterpreting a clause in the Excise Act which reads “having regard to the economic development”.

According to the Excise Act, duty-free vehicle permits cannot be issued to politicians, pensioners, senior government officials, semi government employees, or other dignitaries. The Excise Act doesn’t authorise the issuance of vehicle permits to people serving in such capacities. However, Motor Vehicle Permits on Concessionary Terms continue to be granted to these groups, disregarding the provisions of the Excise Act. During an investigation done by this newspaper it was revealed that these permits are being issued by misinterpreting a clause in the Excise Act which reads “having regard to the economic development”.

The Excise Act specifies that even a President can obtain a duty-free vehicle only during his/her tenure, and it must be registered through the Presidential Secretariat. Such vehicles cannot be registered as a private asset under the President’s name. It must be registered under the name of the President’s office. Despite this, the Minister of Finance has been issuing duty-free vehicle permits to the aforementioned parties by misinterpreting this above mentioned clause. Additionally, duty-free vehicles have been granted to government officials both during their service and upon their retirement. This has resulted in a significant reduction in duty fees. Since the 1990s, politicians, government officials, and dignitaries have denied the country substantial tax revenue by exploiting this clause and importing vehicles. They have misused this clause to gain rights to which they aren’t entitled to. In some cases, such grants and privileges have been made to support the survival of the state or the ruling political party.

Under the Excise (Special Provisions) Act, No. 13 of 1989, plans were made to levy excise duty on vehicles. This was enacted through Extraordinary Gazette No. 633/10 dated 25-10-1990, based on the powers granted to the Minister of Finance under the said Act. The Gazette came into effect on 01-11-1990 following an order issued by the then Finance Minister, D.B. Wijetunga.

Section 2(1) of the Excise Act authorises the Director General of Excise to enforce the Act, and provisions have also been made to appoint a staff to assist in its implementation.

Section 3(1) of the Excise Act states that “There shall be a charge levied and paid on every article manufactured or produced in Sri Lanka, or imported into Sri Lanka, an Excise Duty at such rate or rates as may be specified by the Minister, by Order published in the Gazette. Every such article in respect of which an Order is made under this section is hereafter referred to as “an excisable article”. Excise duty may be levied according to the quantities, percentages and rates specified in the gazette issued by the Minister of Finance; which states the articles that are subject to excise duty as per section 3(1).

Excise duty must be levied on an article once it is classified as subject to excise duty. If the article is manufactured in Sri Lanka, the tax must be paid according to Section 5(1)(a) of the Act. This section stipulates that the relevant tax must be paid within one calendar month following the end of the quarter in which the sale of the article occurred. For articles manufactured abroad, the tax must be paid to the Director General of Customs before the article is cleared from the customs warehouse upon importation to Sri Lanka.

If a customer purchases a necessary luxury or essential article, there will be demand for that article whether it is manufactured domestically or abroad. Based on this demand, a tax is levied according to the article’s economic value. These taxes can then be used for the country’s economic development. Therefore, the Excise Act clearly specifies that taxes should be imposed on every article manufactured or imported into the country.

According to Section 3(c)(1) of the Excise Act, the Minister has the authority to grant tax exemptions based on special reasons or circumstances. The Act states that, “The Minister may, having regard to the economic development of the country by Order published in the Gazette, exempt from the payment of the Excise Duty payable under this Act, any such excisable articles or any such class or description of excisable articles as are or is specified in such Order subject to such condition as may be specified in the Order.”

A portion of the articles subject to excise duty specified therein can be exempted at the Minister’s discretion, provided the conditions for excise duty payment are met. However, under Section 3(c)(3) of the Act, if the exempted party fails to adhere to the conditions, the exemption will be revoked, and the full tax amount must be paid by the person of the company. Nevertheless, the permits mentioned above have been issued misinterpreting the “having regard to the economic development” clause, without including these conditions or any mention of them.

Exemptions from excise duty

In addition to the provisions mentioned earlier, there are several other exemptions from excise duty. Section 3(a)(1) of the Act states that the representative in Sri Lanka of the Government of any foreign state, or persons on the staff of any such representative, representatives of the United Nations, its affiliated organizations, or representatives of international organizations, are exempted from the payment of excise duty on excisable articles cleared out of customs bond by or for the use of such representatives, based on several conditions. Furthermore, Section 3(b)(a) allows for the exemption of articles cleared from customs bond for the official use of the President. Section 3(b)(b) of the Act also provides that articles of every description purchased or procured from a customs duty-free shop are exempted from the payment of duty.

Additionally, according to section 5(3)(1) of the Act, articles which has been produced or manufactured in Sri Lanka for the purpose of export, shall not be liable for the payment of excise duty, if a bond is executed for the landing of such excisable article at the port of destination, and if the foreign exchange is transmitted to a local bank as per Extraordinary Gazette No. 636/3 dated 11-13-1990 and regulation No 03 of 1990. Moreover, as outlined in Section 5(3)(ii) of the Act, an excisable article imported for the purpose of being used as raw material in the manufacture of articles for export by exporters, shall not be liable for the payment of excise duty if sufficient proof is furnished that such manufactured article was manufactured for export.

|

- Senior Attorney-at-Law Gamini Ekanayake |

Senior Attorney-at-Law Gamini Ekanayake commented as follows: “Excise duty is the amount payable by the producer or importer on an article. According to Section 12(a) of the Act, any penalty due to non-payment is also considered part of the excise duty. The Excise (Special Provisions) Act No. 13 of 1989 was enacted, and later, by Act No. 40 of 1990, Section 3 was amended and reintroduced as Sections 3(a) and 3(b). By Section 3(a) the Minister from time to time, by Order published in the Gazette exempted several articles from payment of excise duty. Specifically, Section 3(a)(i) of the 1990 amendment exempts the importation of vehicles for foreign agents from excise duty, with the applicable tax rates specified. According to section 3(b) vehicles and articles for the official use of the President, and all articles purchased from Custom Duty Free Shop are also exempt from excise duty,” he said.

The Excise Act No. 8 of 1994 is a significant act. Section 3(c) of this Act states, “The Minister may, having regard to the economic development of the country”. However, according to Ekanayake, this clause appears to be frequently misused. It is unclear whether the clause “The Minister may, having regard to the economic development of the country….” is used for the purpose of a national organization. The Gazettes issued so far suggest that the Finance Ministers from the 1990s to the present have misapplied this provision. For instance, in 2016, as Finance Minister of the 8th Parliament, Ravi Karunanayake issued permits to all MPs, merely charging CFI. Similarly, during Mahinda Rajapaksa’s tenure, various individuals, government officials, dignitaries and institutions were granted tax-free vehicle permits.

Accordingly, former Finance Ministers have acted in violation of the purpose of the Excise Act. The Minister has issued gazettes using the powers granted by the amended Act No. 8 of 1994, but this discretion has been misused under the pretense of contributing to the country’s economy. As a result, a significant amount of tax revenue has been lost. If issuing tax-free vehicle permits genuinely contributed to the country’s economy, the recipients of those permits would still be using the vehicles. However, this is not the case; they have sold their vehicle permits.

If vehicle permits are sold in this manner, the tax can be recovered under the Act. The government should focus on whether they can recover that money even if authorised under Section 3(c)(III) of the Act.

Failing to enforce such taxation would constitute a violation of the people’s sovereignty and misinterpret and infringe upon their fundamental rights. “Any citizen has the right to file a fundamental rights case in the Supreme Court to challenge this issue. What is occurring here is a misuse of the Minister’s discretion, as provisions of the Act are being exploited through Gazettes. The Minister has the authority to issue these notifications, but this power should only be used to contribute to the country’s economic development. Providing duty-free vehicle permits doesn’t contribute to the economy through tax exemption. If those who received vehicle permits for economic development still had those vehicles, it could be said that they contributed to economic growth. However, these permits are often sold within a year, which is problematic. The Minister’s actions are infringing upon the basic rights of the citizens and violate the constitution.

“If that is the case, it appears that Finance Ministers, Ministry Secretaries, or other high officials in this country have not properly studied the clauses of the Excise Act. It is important to examine which articles are exempted from duty and how these issues have impacted both the country’s economy and the general public, particularly concerning the implementation of orders and plans related to tax exemptions for certain articles. Such an inquiry may reveal that some decisions made by Finance Ministers have been unfavourable and illegal. The officials in the Ministry of Finance responsible for enforcing the law also share responsibility for this issue” he said.

According to him, additionally, Section 3(c)(1) of the Act does not define “economic development.” He said, “The Finance Minister has exploited this lack of definition to grant tax concessions contrary to the provisions of the Act. The country has lost a significant amount of tax revenue due to the provisions in the Excise Act being left to the discretion of the Finance Minister. This is a result of illegal tax exemptions and insufficient tax collection. This is confirmed by Extraordinary Gazette No. 2364/36 dated 31 December 2023 and Extraordinary Gazette No. 1119/6 dated 14 February 2000.

“It appears that Extraordinary Gazettes numbered 2312/68, 2312/67, 2113/11, 2176/19, 2366/19, 2376/14, 2113/9, 1992/30, 2222/2, 2046/11, 2044/32, 2239/16, 2047/15, and 2068/19 have acted contrary to the provisions of the Excise Act. There have been instances where previous orders were canceled and new orders were included in subsequent gazettes,” he said.

Tax exemptions and reductions continue to occur across various fields today. The exemption of excise duty and issuance of permits for vehicle imports have been granted based on the seniority and position of government officials. Ideally, tax relief should be applied equitably to everyone, but the same system has not been consistently applied when issuing excise duty-free vehicle permits. This is evident from page 54a of Extraordinary Gazette No. 2312/68 issued on 2022-12-31. The ongoing issuance of tax concessions and tax-free vehicle permits constitutes a violation of the Excise Act.

“When ambulances or other vehicles are received from other countries in the event of a disaster, excise duty must typically be charged on those vehicles. However, when these vehicles are given as a grant, the donating countries are usually unwilling to pay the excise duty. Considering the economic development benefits, these vehicles could be exempted from excise duty. After completing their assigned tasks, the vehicles should be returned to the donor countries. Alternatively, if the vehicles are taken over by the government and auctioned, the buyers should be required to pay the excise duty. For projects receiving such vehicles, an exemption from excise duty may be granted considering the economic development. Once the project is completed, the vehicles should either be depreciated or appropriately documented by the relevant line ministry or departments. Criteria can be included for these documents,” he added.

In the past, 2,000 three-wheelers were brought to Sri Lanka for the police and were exempted from excise duty. This exemption was inappropriate. Although the three-wheelers were intended as an investment for the government, they were exempted from excise duty by misapplying clauses meant to support economic development. According to Section 3(6) of the Act, whether imported by the government, on behalf of the government, or produced domestically, excise duty must be paid. This is why fuel is taxed after being imported into the country. However, Section 3(6) of the Act was violated by Extraordinary Gazette No. 2222/2 issued on 2021-04-05 and Gazette No. 2239/16 issued on 2021-08-03. Similarly, 62 double cabs and 52 water bowsers were also imported in violation of the Act.

In a context where “economic development” is not properly defined, tax concessions, tax-free vehicle permits, and reduced tax collection are implemented using different interpretations of this clause. “Against such backdrop, duty-free vehicle permits are issued to politicians, senior government officials, members of the security forces, professionals, and dignitaries. Such practices constitute a violation of the Excise Act. On November 10, 2016, Extraordinary Gazette No. 1992/29 removed the barriers to tax concessions, leading to an increase in the issuance of tax-free vehicle permits and tax concessions granted at discretion after 2016.

“Another important point to note is that those who issued such circulars and gazettes are often motivated by the desire to obtain the privileges that the Act has forfeited. Page 54A of Extraordinary Gazette No. 2364/36, issued on December 31, 2023, details that public officers using a permit under Public Administration Circular 22/99 are classified according to the following amendments based on their positions as specified in the circular,” he said.

In the Gazette, government officials are categorized as I, II, and III according to their rank. The Gazette also outlines the tax concessions available to officials in each category. Accordingly, a tax deduction of 22 million rupees has been granted for vehicle permits to government officials in Category I, 16 million rupees for Category II officials, and 12 million rupees for Category III officials.

Additionally, using the Motor Vehicle Permit on Concessionary Terms issued under the amended Trade and Investment Policy Circular No. 01/2018 dated 15-2018, a concessional vehicle permit worth 3.6 million rupees was granted to a government official. Similarly, a Sri Lankan diplomatic officer who serves in foreign missions receives a tax relief of 3.6 million rupees using a permit issued by the Ministry of External Affairs, according to amended Circular No. 210 (iii). Exporters with an export value of at least 200,000 USD, who export up to 20 motor vehicle units that are at least five years old and have a CIF value not exceeding 50,000 USD, are granted tax relief on their vehicle permits issued by the Secretary of the Ministry of Finance, based on the recommendation of the Ministry Secretary. Only 50 percent of the vehicle’s value should be paid to the line ministry in charge of industry. Additionally, under Local Government and Provincial Council Circular No. 01/2017 dated 21-04-2017, a councilor representing those institutions is required to pay 35 percent of the vehicle’s value.

“Politicians may argue that tax concessions and duty-free vehicle permits are granted via gazette notifications considering economic development. However, this claim doesn’t align with the actual situation. Instead, these practices constitute a breach of the Excise Act. It is imperative to evaluate whether the continuation of these practices will lead to a significant loss of tax revenue that belongs to the country” said Ekanayaka.