Reply To:

Name - Reply Comment

Former MP Patali Champika Ranawaka contends that despite promises made before the elections, to reduce the prices and taxes on fuels, it has not happened. He supports this claim by citing the difference between the import and market prices of the fuels, which he attributes to taxes.

Former MP Patali Champika Ranawaka contends that despite promises made before the elections, to reduce the prices and taxes on fuels, it has not happened. He supports this claim by citing the difference between the import and market prices of the fuels, which he attributes to taxes.

To verify the claim, FactCheck.lk consulted the Fuel Price Tracker (FPT) by PublicFinance.lk

The statement made by the former MP is problematic for two reasons.

First, the statement derives the tax by simply subtracting the import price from the market price. However, the difference between these two prices includes more than just taxes. It also includes other costs associated with fuel supply, including storage, transport and retailing. In 2018, the Ministry of Finance published a cost-based fuel price formula — which includes the other costs and taxes. Based on this formula, actual taxes for October amount to LKR 124.6 and LKR 93.9 for petrol and diesel, respectively. The statement cites a much higher cost of importation than what is used in the formula. Therefore, the former MP using his methodology, which does not count other costs, arrives at a lower tax amount than the actual tax—which is calculated from the actual costs.

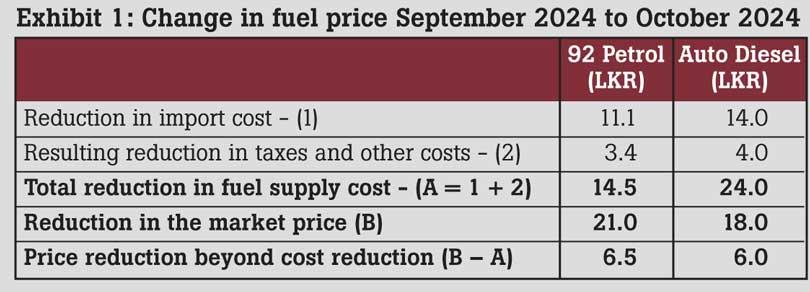

Second, the tax structure on fuel is established by law, and has not been formally adjusted. However, the FPT shows that the prices of petrol and diesel were decreased by LKR 21 and LKR 18, respectively. Part of this reduction can be attributed to a reduction in cost, in two ways: (1) likely reduction in importation cost, as the Singapore PLATTS price for petrol and diesel reduced by LKR 11.1 and LKR 14.0, respectively, and (2) a corresponding reduction in total tax, as VAT is charged as a percentage of import cost. However, as shown in Exhibit 1, the decreases in price were more than the sum of these cost reductions. Therefore, the MP’s claim, that there was no reduction in price and tax, is inaccurate in two ways. Firstly, the price has been reduced by more than the reduction in cost. Secondly, the tax amount has reduced through reduced VAT on the reduced import cost. Moreover, the MP’s calculation of taxes, based on the figures he claims for the cost of importation, is also incorrect.

Therefore, we classify the former MP’s statement as FALSE.