Reply To:

Name - Reply Comment

Although Sri Lanka has a meagre track record of attracting foreign direct investment (FDI), data indicate that the very little FDI Sri Lanka receives yields good profits for the investors.

Although Sri Lanka has a meagre track record of attracting foreign direct investment (FDI), data indicate that the very little FDI Sri Lanka receives yields good profits for the investors.

In fact, the data suggest that the success of these FDI ventures probably contributed to the deterioration of the balance of payment (BOP) in the country. This is due to a high volume of profit repatriations by FDI ventures – especially during the last few years.

Many developing countries have experienced similar phenomena. Even large FDI recipient countries like India have experienced weakening of the BOP, due to a high volume of profit repatriations by FDI ventures in the recent past.

FDI profit growth

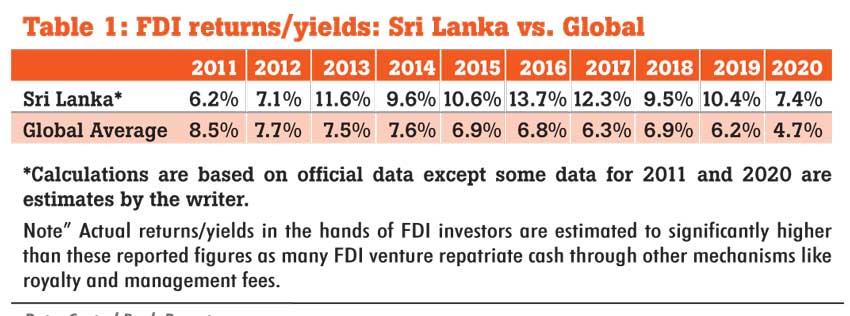

The profits of Sri Lanka-based FDI ventures have seen a notable increase during the last decade. Interestingly, the returns of Sri Lankan FDI ventures have steadily increased while the global (average) FDI returns have declined.

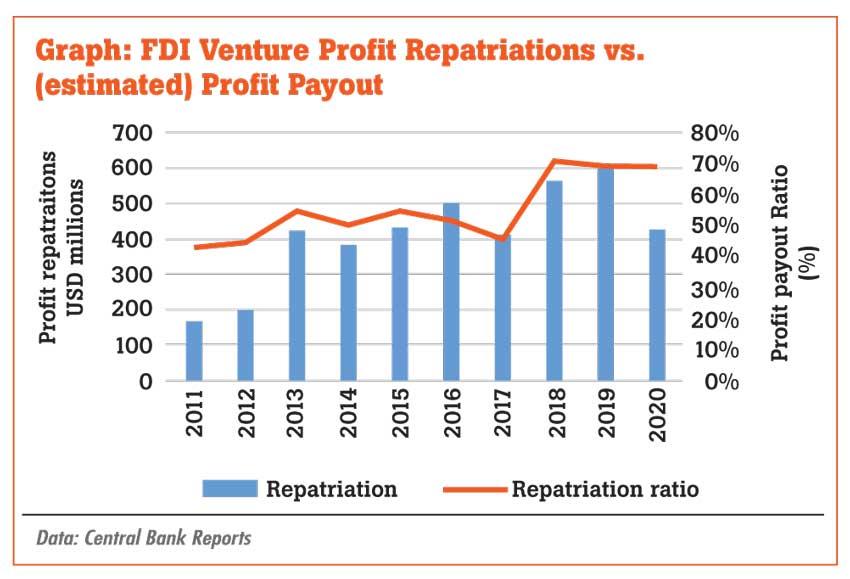

An increase in profit leads to higher dividend outflows. As shown in the graph, both dividends and (estimated) profit payout ratios have increased during the last 10-year period. It should be noted that the profit repatriations have increased unusually during the last three years. This indicates that the majority of FDI ventures were reluctant to reinvest/expand in Sri Lanka or majority of the FDI ventures are reaching the last stage of the FDI cycle (i.e. repatriation stage).

A decade of negative FDI cash flows?

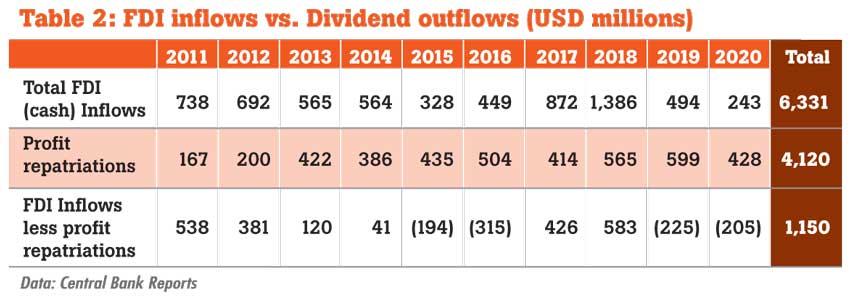

Sri Lanka’s economic policies always place high hopes on FDI inflows to bridge the country’s endemic BOP gap. However, the data suggest that even the very little FDI Sri Lanka attracts is probably contributing to deteriorate the BOP further.

For example, during the last decade, Sri Lanka attracted US $ 6.3 billion (see Table 2) as FDI inflows (money coming into the country) while dividend outflows from FDI ventures amounted to US $ 4.1 billion, with a net benefit of only US $ 1.1 billion (which is ironically equivalent to the proceeds Sri Lanka received from the sale of the Hambantota Port). Even this net benefit is likely to be negative, if we include the debt settlements and interest payments on the offshore private loans obtained by these FDI ventures.

Profits growth from non-tradable sector?

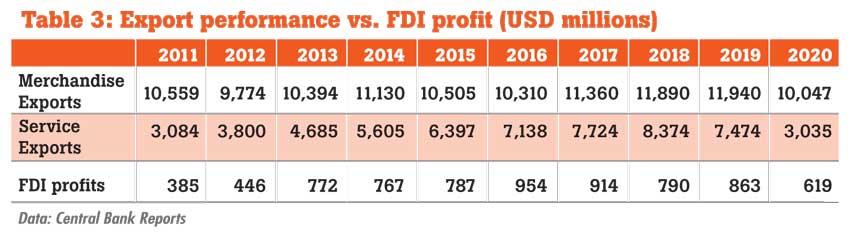

Even having a negative FDI cash flow is still beneficial to Sri Lanka, if these FDI ventures generate foreign income to the country and use significant local resources as inputs (or local value addition). However, Table 3 suggests that the profit growth of the FDI ventures during the last decade is probably driven by neither the merchandise exports nor service exports.

This trend is in line with the fact that the majority of FDI Sri Lanka attracted during the last decade is into non-tradable industries, which probably increased the imports rather than increasing the exports.

High payouts from real estate ventures?

Judging by the overall FDI cash flow trends, it is probable that the (overall) increase in the FDI ventures’ profits was mostly driven by the non-tradable industries like real estate development, which tend to have irregular and high profit repatriation patterns (with low reinvestments).

High profit repatriations during the second half of the last decade appear to be the profit made by foreign investment into real estate projects during the first half of the last decade (post-2009 investment boom).

Gradual expansion of the BoP gap during the last 10 years is probably hastened by the growth in real estate development, which utilises a high level of imported inputs (materials and labour), with no corresponding foreign revenue.

Selling national assets to finance FDI dividends?

The data clearly suggest that Sri Lanka’s increasing BOP crisis is at least partially linked to the nature of Sri Lanka’s FDI, which are concentrated in non-tradable industries. Nonetheless, Sri Lanka still continues to actively solicit FDI into non-tradable industries like real estate development. This is evident from the extensive pipeline of lands the government is offering for investors to develop further mega projects.

Sri Lanka’s BoP may get worse, if this policy continues and Sri Lanka may be compelled to sell profitable national assets to foreign investors to periodically find dollars to support the high profit outflows and import demand of these non-tradable FDI ventures. For every FDI dollar Sri Lanka receives for real estate projects, Sri Lanka’s BOP is likely deteriorating by several dollars.

(Indika Hettiarachchi is an independent international advisory professional in private market investment and projects. He has an MA in Economics from the University of Colombo and a BS in Management from the University of Wisconsin. He can be reached at [email protected])