.jpg) A recent report released (March) by the International Rubber Study Group (IRSG) indicates that the stock balance of the global natural rubber industry at the end of 2013, specifically that of the Asia Pacific region, is in a position of production exceeding that of consumption by 3,020,000 tonnes, which may be a worrying factor to the producers in terms of natural rubber (NR) prices in the immediate future.

A recent report released (March) by the International Rubber Study Group (IRSG) indicates that the stock balance of the global natural rubber industry at the end of 2013, specifically that of the Asia Pacific region, is in a position of production exceeding that of consumption by 3,020,000 tonnes, which may be a worrying factor to the producers in terms of natural rubber (NR) prices in the immediate future.

Total rubber consumption

Total world rubber consumption continued to grow in Quarter 4, 2013, however at a sharply decelerated rate. The deceleration is a reflection of the rubber industry adjusting to the relatively robust rate of expansions in Quarters 2-3, 2013, specifically the Asia-Pacific region. The average Quarter 2-3 share of total annual consumption was 49.8 percent in the 2011-2012, while it was 50.8 percent in 2013 for Asia-Pacific. Neither the leading economic indicators (industrial production index) nor Quarter 4, 2103 gross domestic product (GDP) growth rates from across the major rubber consuming regions suggest economic slowdown as the reason.

The Quarter 4, 2013 negative growth in the US does not reflect the macroeconomic status of the country. It instead represents the combined impact of continuing growth in imports of tyres and a slowdown of the replacement tyre sales in the quarter, following the strongest six consecutive month growth since January-June 2010, led decrease in demand for rubber from the passenger car tyre sector.

The consumption of rubber has been slowing down in EMEA, mainly localised to Russia, but the 8.6 percent decrease in Quarter 4, 2013 is not a wholly accurate reflection of the health of the rubber industry of the region. The size of the downturn is mainly technical and due to an anomalous December 2012 data.

Natural rubber consumption

The world NR consumption increased for Quarter 4, 2013, but at a decelerating rate. The industry adjusting to the relatively robust rates of growth in Quarter 2-3, 2013 is the reason for the deceleration.

The rate of deceleration was at a faster rate as compared to the total rubber consumption. The NR price (SGX’s TSR 20) has been at a discount to the SR price (US export unit value of SBR) since March 2013, while the output of commercial vehicle tyres (the single largest user of NR) appeared to have increased at an accelerated in Quarter 4, 2013

Using the exports data of China as a proxy for global production of commercial vehicle tyres, where it increased by 22.6 percent as compared to 18.6 percent in Quarter 3, 2013, the growth rate of NR consumption in Quarter 2-3, 2012 was lower as compared to the total rubber consumption over the same period and the supply of NR was in excess of demand, with this position being easier in Quarter 4, 2013, which all should indicate the NR consumption performing comparatively better. While a definitive answer is currently beyond reach, a speculative one points to the relative price, which moved against NR in Quarter, 4 2013, increasing to an average 94.8 from 87.9 in Quarter 3, 2013.

Natural rubber production

World NR production increased at a sharply accelerating rate in Quarter 4, 2013. It is the fastest growth rate since Quarter 1, 2010, when the global rubber industry was starting its recovery from the 2008-2009 world economic recession-driven downturn. Mechanically, the acceleration was driven by Indonesia and Thailand (Table 1).

The Quarter 4, 2013 output of Thailand is the largest for any given quarter in the history of NR industry for any single country and the November-December 2013 production is also the first time a 400,000 tonne mark had been breached on a monthly basis. The ability to meet the accelerated growth in output from Thailand is largely explained by the combination of the increase in the total tappable area for the country and the equally sharply accelerated imports demand, mainly from China, which increased by 50.0 percent. Quarter 4, 2013 Thailand’s exports into China were 700,615 tonnes, with the October volume breaching the 200,000 tonnes mark for the first.

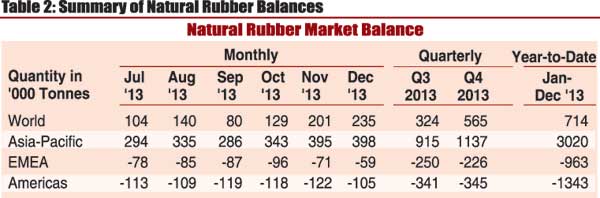

Rubber balances and stocks

The accelerated growth in NR production, which was mainly responding to imports demand from China, in the face of decelerated NR consumption created a surplus in the world NR market in Quarter4, 2013.

The latest market balances for the three NR growing regions are given in (Table 2).

Natural rubber market activities

-

Futures markets price activities

Since December, NR spot and benchmark prices have been continuously falling. The price drop has been largely blamed on increased Chinese stockpiling and a slowdown in Chinese manufacturing. In line with dropping prices, the daily turnover at the Shanghai futures market (SHFE) also decreased continuously.

Markets have been in contango, however Tokyo futures exchange (TOCOM) moved to backwardation during the end of last year and the beginning of this year, which is possibly due to demand insufficiencies. Contango was abnormally large at SHFE during September and October but subsequently narrowed down.

Economic indicators

-

Recent economic development

Most of the advanced economies are still recovering and growth is still looking relatively bullish.

Japan’s economy grew by 1.7 percent in 2013 and it is projected to grow again by 1.7 percent this year. The Euro area GDP became more positive towards the end of 2013 and overall it dropped by only -0.4 percent. However, it is projected to grow by 1 percent in 2014 and by 1.4 percent the following year. The United States continues its bullish trend and it is forecasted to grow by 2.8 and 3 percent in 2014 and 2015, respectively.

Although economic growth in emerging markets has been poised to slow down, the last quarter of 2013 has seen a positive momentum. China’s economy rebounded towards the end of 2013. However, India has seen relatively sluggish growth, Russia’s economy is going through its worst slowdown since the 2009 economic crisis and Latin America is only slowly recovering from the regional recession.

Asia

Although IRSG’s leading indicator of China’s economy (rail freight traffic) has slowed down, it remained positive towards the end of 2013. There is some indication of a current Quarter 1, 2014 slowdown as HSBC’s reports. PMI of the Chinese private sector has dropped to 48.5 in February and 48.1 in March, which is below 50 and is indicative of an economic contraction.

Japan’s industrial output continues to be on an upward trajectory and yet the overall economic output has lost some momentum in early Quarter 4, 2013. Although a lax monetary policy (informally phrased as Abenomics) has buoyed this economic expansion, the continuation as well as the effect of this economic policy, will have run its course by the middle of this year and Japan’s economy is projected to slow down to 1.7 and 1.0 percent in 2014 and 2015, respectively. Growth might be spurred again, if the Japanese government increases its fiscal spending as recently promised in the press.

Although the Euro area GDP growth has been largely negative in the last few years, it picked up towards the end of 2013 and the industrial production has been more bullish recently. However, this is still largely driven by Germany. As the Euro crisis has started to improve, future positive growth in the Euro area will also be propped up by former sovereign debt crisis countries. Further growth is unlikely to set in, as the European Central Bank (ECB) has announced that positive economic growth makes more accommodative monetary policy unlikely.

Americas

Americas

Economic growth continues to be robust in the United States and this is supported by industrial production data as well as a positive PMI. As GDP growth continues to be strong, the US Federal Reserve Board is expected to reduce its asset buying programme. This is in line with an improved labour and housing market.

Brazil’s Central Bank has continued to tighten its monetary policy increasing its policy interest rate as inflation is rising and industrial production has dipped in December 2013. Mexico’s industrial production has remained steady and a strong US economy will support this development.

Summary

Most of the advanced economies are still recovering and growth is still looking relatively bullish. Japan’s economy grew by 1.7 percent in 2013 and it is projected to grow again by 1.7 percent this year.

Total world rubber consumption continued to grow in Quarter 4, 2013, however at a sharply decelerated rate.

World NR production increased at a sharply accelerating rate in Quarter 4, 2013. It is the fastest growth rate since Quarter 1, 2010, when the global rubber industry was starting its recovery from the 2008-2009 world economic recession-driven downturn.

The accelerated growth in NR production, which was mainly responding to imports demand from China, in the face of decelerated NR consumption created a surplus in the world NR market in Q4 2013. World SR market was in 30,000 tonnes surplus in Quarter 4, 2013.

Since December NR spot and benchmark prices have been continuously falling. Prices on the physical markets followed the trend of the futures markets.

Rising supply, weak demand and poor refining margins have been blamed for a slight drop of Brent Crude to almost US $ 106/barrel in January 2014.

Global NR latex consumption continued to grow at a decelerating rate reaching 1.4 million tonnes in 2013. A relatively robust acceleration was seen in Quarter 4 across the emerging markets as wells as in the developed markets. Among producers in the Asia Pacific region, latex production increased in Thailand and China, while production dropped across Malaysia, India and Sri Lanka driven by adverse weather conditions.

Exports of selected latex products continued to increase in Quarter 4, 2013, led by the all-important, in terms of volume of latex used, gloves. A combination of the renewed threat from the confirmed human infection with avian flu and continued fall in the cost of raw material (latex) appear to be behind the accelerated increase of Quarter 4, 2013 (Reference: Rubber Industry Report of IRSG, March, 2014).

(N. Yogaratnam can be contacted at [email protected])