Reply To:

Name - Reply Comment

By Indika Hettiarachchi

.jpg) Sri Lankan enterprises – especially SMEs use a comparatively high level of bank borrowings to fund investments. This is partly due to low level of domestic savings and inefficiency in the capital market.

Sri Lankan enterprises – especially SMEs use a comparatively high level of bank borrowings to fund investments. This is partly due to low level of domestic savings and inefficiency in the capital market.

Bank borrowings account for a significant percentage of FDI as well. A reduction in borrowing and increasing equity funding can help Sri Lankan enterprises become more competitive and grow faster. Increase in equity investments can also improve country’s capital stock and wealth.

Use of debt to fund private sector investments

According to the Sri Lankan Enterprise Survey carried out by the World Bank (2011), 43.6 percent of Sri Lankan enterprises use (bank) borrowing to finance investments, and on average 35.4 percent of new investments are funded by bank borrowings compared to the South Asia average of 19 percent and world average of 16.5 percent (Table 1).

Medium-sized firms borrow more compared to small and large firms. However, when we compare Sri Lankan firms’ borrowing data with regional and global data, higher level of borrowings in both Small and Medium sized enterprises (“SME”) is evident. Survey results also highlight that Sri Lankan firms rely heavily on bank borrowings to finance working capital too. Use of retained earnings and equity to fund new investments seems low among Sri Lankan firms—especially considering the age/maturity of Sri Lankan firms (Table 2).

.jpg)

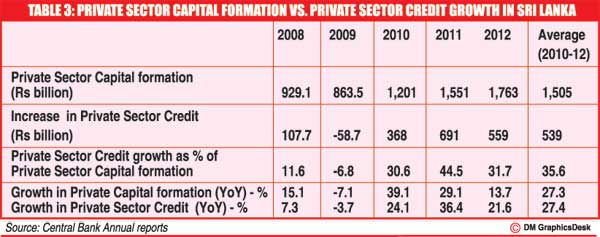

We can verify the above survey findings by analyzing Sri Lanka’s private sector capital formation and private sector credit growth data as well. As shown in Table 3, Sri Lanka’s average annual (nominal) private sector capital formation (i.e, total private investments) during 2010-2012 amounted to Rs.1,505 billion, while average annual (absolute) growth in private sector credit during the same period amounted to Rs.539 billion.

Average (absolute) growth in credit is equivalent to 35.6 percent of average annual private sector capital formation. This suggests that approximately 1/3 of private sector investments are funded by credit. Since private sector credit includes personal credit (which is around 30 percent of total private sector credit), and private capital formation includes non-business related capital spending, this is not a perfect measure.

Nevertheless, we can still argue that approximately 1/3 of private sector investments are credit funded. Furthermore, the average annual growth of private sector credit during the three year period from 2010 – 2012 was 27.4 percent— which is almost same as the 27.3 percent average annual growth rate in private sector capital formation during the same three year period.

High levels of debt are seen even in listed companies too. Out of the 222 listed non-financial sector companies in the Colombo Stock Exchange (CSE), 40 percent have more than 35 percent gearing. As a country with national savings-investment gap of 4.2 percent of Gross Domestic Product (GDP), Sri Lanka relies heavily on Foreign Direct Investments (FDI) to drive the economy. Close analysis of FDI data reveals that significant percentage of FDIs also represents borrowings from banks. In 2012, US$ 440 million or nearly 33 percent of total US $ 1,338 million FDIs were bank borrowings (Table 4).

.jpg)

Drawbacks in using high borrowings

Leverage of 1/3 or even more is appropriate in some instances where growth and profitability justify such leverage. Although high borrowings improve the return on equity capital, high borrowing can also increase overall risk of the firm and prevent it from growing. High borrowings decrease profits, and exert pressure on free cash flows. High borrowings results in transfer of larger proportion of wealth creation or value addition of an enterprise to lenders (or banks) instead of equity holders or owners. This can result in lower capital accumulation overtime by entrepreneurs.

Lower capital accumulation leads to inefficiency and make companies less competitive—due to the ensuing incapability to invest in new technology or expansions to enjoy higher economies of scale or lower costs. High leverage prevents companies from growing to its full potential, as it will be difficult to undertake more risks (i.e., new projects) with a leveraged balance sheet. High borrowings also make companies vulnerable for external shocks.

In entrepreneurial economies, business owners make returns not only from profits earned from the businesses, but also through appreciation and realization of value of their businesses. High borrowings can prevent entrepreneurs from achieving returns from appreciation of the value of a business. This is because of the negative impact on borrowing on growth, profitability and also on long term sustainability – all of which are important elements driving the value of an enterprise.

Review of Sri Lanka’s case

It is very difficult to estimate the impact of high level of debt finance in Sri Lankan companies on their growth (in the past), and its impact on the economy. However, we can compare borrowing data of Sri Lankan enterprise with the borrowing data of other high growth-countries/ regions, and infer possible causes and consequences of same.

As shown in Table 1, firms in China and East Asia have very low levels of borrowings compared to Sri Lanka. Furthermore, the average real growth rates of companies in these regions are higher than Sri Lanka’s. Hence, we can reasonably argue that the low level of borrowings in China/East Asia have contributed to the higher economic growth witnessed in these countries/region. Sri Lanka experienced high level of interest rates throughout (until 2009). Hence it is possible that high interest rates combined with high loan stock have most likely hindered growth of local enterprises, and hence overall economic growth of the country.

As mentioned earlier, the Enterprise Survey results highlights that Sri Lankan SMEs use high level of bank borrowings—especially medium-sized firms which fund on average 53.5 percent of new investments using bank loans. This is very high compared to regional average of 18.5 percent and global average of 17.8 percent (in 2011). SMEs in Sri Lanka contributed estimated 40 percent to GDP during 2010-2012, and hence it is likely that the potential negative impact on GDP growth stemming from the high borrowings in SMEs was significant.

Sometimes high borrowings are a consequence of high growth in business. During 2010 and 2011 Sri Lankan economy grew by 8 percent and 8.2 percent respectively – highest GDP growth rates recorded in over three decades. Loans to SMEs grew by 68.3 percent in 2011 (according to Ministry of Finance Annual Report). Hence it is clear that high level of loans in medium-sized firms (as reflected in 2011 Enterprise Survey) is probably associated with the escalation of business activity in 2010-2011.

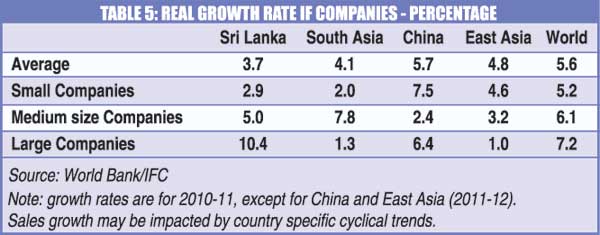

However, such increases in borrowing or over trading situations need to be supported with equity infusions in order to reduce financial risk of borrowers, and also to make sure growth is sustainable. Yet the real growth of business in Sri Lankan SMEs during 2010-2011 period lagged growth rates recorded in other growth regions/countries (Table 5).

Sri Lankan firms use comparatively lower level of retained earnings and equity to fund new investments. This is due to combination of several factors. One contributory factor is that firms and/or entrepreneurs have not been able to accumulate enough internal capital/ resources. This is again linked to lower growth, lower profitability and also to high debt burden itself - which could have drained out firms’ value addition to lenders.

Sri Lankan firms have recorded a real growth of 3.7 percent in 2010 – 2011 period (when the Enterprise Survey was carried out) compared to regional average of 4.1 percent and global average of 5.6 percent. Sri Lanka’s large enterprises which use 56 percent more gearing (to fund new investments) than global average have attained higher growth compared to small and medium sized firms. Small firms which use almost 100 percent more gearing than global and South Asia benchmark have achieved only a 2.9 percent real growth. Mid-sized enterprises which use more than 200 percent gearing to fund new investments (compared to regional and global average), have performed relatively better. But they have lagged behind regional peers. Furthermore, as shown in Table 2, average age of a Sri Lankan enterprise is 23.2 years— 50 percent more than regional and world average. It is also likely that majority of Sri Lankan enterprises have passed their initial growth stages of their life-cycle. When we consider the age (maturity) of Sri Lankan companies vs. their use of borrowings, it further proves that use of high bank debt probably constrained their growth in the past and prevented them from accumulating internal capital.

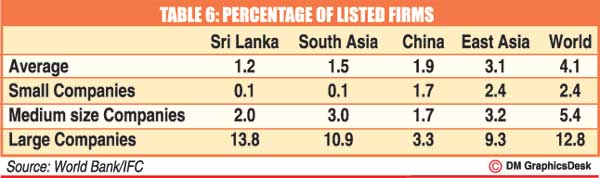

Another reason for high bank borrowings in Sri Lanka is the non-availability of (external) equity funding. Even though this is broadly linked to the low level of domestic savings in the country, the inefficiency in the capital market has also contributed for this. Capital market has failed to efficiently channel savings into equity investments, and Sri Lanka’s equity capital market is only focused on listed stocks. There is only handful of investors focusing on investing in SMEs or private companies. Private Equity and Venture Capital activities are very low in Sri Lanka. According to the Enterprise Survey, only 1.2 percent of Sri Lankan firms are listed/public firms compared to global average of 4.1 percent (Table 6).

Although a higher percentage (13.8 percent) of Sri Lankan large enterprises are listed in the CSE, percentage is very low for SMEs. Only 2 percent of medium-sized firms are listed in Sri Lanka compared to 3 percent in South Asia and 5.4 percent globally. This shows a potential for many Sri Lankan SMEs to become listed companies, especially given their maturity/age. When a firm is listed it is comparatively easier to raise equity as well as debt at favorable terms.

Easy bank credit can also encourage firms to use more credit to fund investments. There has been tremendous growth and innovation in bank lending programs in Sri Lanka. There has been high growth in SME lending schemes—often backed by low cost funding from multilateral lending agencies and international development finance institutions. However, competition in the banking and financial services sector can sometimes lead to irresponsible and inappropriately lending practices which can result in borrowers getting into debt-trap situations thus making borrowers gradually erode their sustainability. It is not possible to sustain a growth with bank credit only. Bank credit can provide short to medium term bridging capital, but adequate level of equity funding is needed to make companies strong, especially if they competing in the international market.

Another cause which may have favoured borrowings vs. (external) equity finance is high inflation prevailed throughout (until 2009). This is because real cost of borrowing declines during inflationary period. Impact of taxes on borrowing for new investments is not very significant in Sri Lanka as many new ventures or projects enjoy tax breaks.

Finally, another factor which may have contributed to high borrowing is the unwillingness of promoters/companies to dilute ownership, which can also be linked to inefficiency of the overall capital market for not popularizing equity investments. Given the age profile of Sri Lankan enterprises, broad-basing equity ownership may be necessary to ensure long term success of local firms.

Need to increase equity investments

Foregoing review clearly shows that Sri Lankan companies need to focus more on raising equity capital to achieve sustainable growth and remain competitive. As Sri Lanka aims to fast track its domestic investments from current 30 percent of GDP to 35 percent of GDP, it is essential that new investments are funded with appropriate level of equity to make sure of achieving the target 8 percent GDP growth. The low inflation and low-tax environment that is currently prevalent in the country also makes it advantageous to use more equity.

Equity investors (non promoters) take long-term view of the business and primarily target to achieve return from capital gains over medium to long term– unlike lenders whose main criteria of lending is the security of the loan or ability of borrower to service the loan in the short to medium term. A healthy capital gain from an equity investment is possible only if the business is profitable and has sustainable growth prospects over long-term. Hence it is natural that equity investors have a commitment to ensure long-term success of the enterprise they fund while sharing risks and rewards equally with the promoters. Hence popularizing more equity investments can help Sri Lanka to achieve higher capital stock and increase wealth of the country.

(The writer is the founding Managing Director of Jupiter Capital Partners – a south Asia focused Private Equity firm. He is a graduate (B.S.) from University of Wisconsin, USA, completed a Masters degree (M.A.) in Economics at University of Colombo, and also qualified as a Chartered Financial Analyst (CFA).

Email: [email protected])