31 Jul 2024 - {{hitsCtrl.values.hits}}

Premier blue-chip company John Keells Holdings PLC reported a decline in group profitability for the first quarter of the financial year 2025 (1Q25) due to pre-opening expenses and non-cash exchange losses of its upcoming high-profile property, and a notable deferred tax credit at the ports and shipping business.

Premier blue-chip company John Keells Holdings PLC reported a decline in group profitability for the first quarter of the financial year 2025 (1Q25) due to pre-opening expenses and non-cash exchange losses of its upcoming high-profile property, and a notable deferred tax credit at the ports and shipping business.

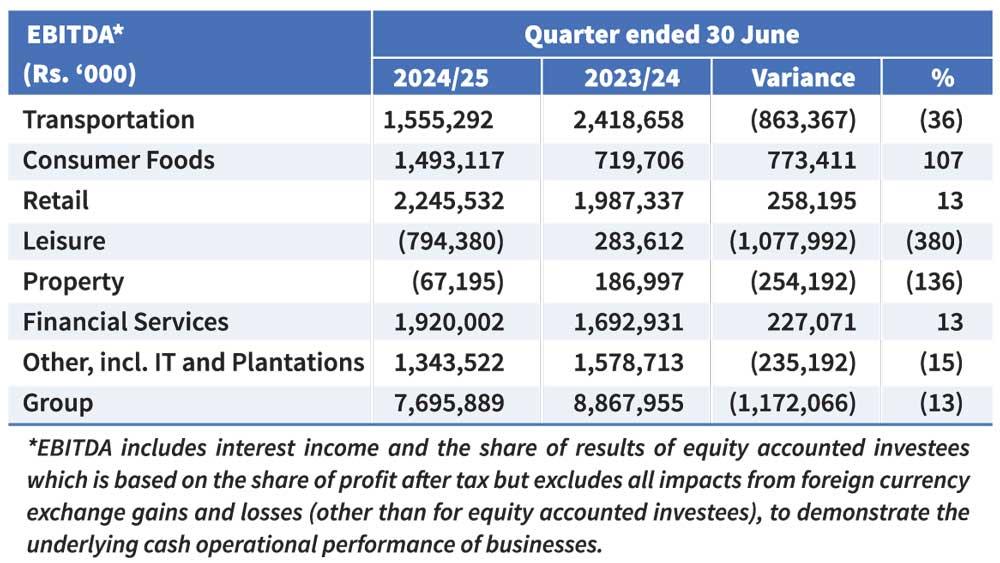

John Keells Holdings saw its 1Q25 group EBITDA contract 13 percent YoY to Rs.7.70 billion.

“The group EBITDA includes substantial pre-opening costs pertaining to the ramp-up associated with the opening of the ‘Cinnamon Life’ hotel at ‘City of Dreams Sri Lanka’, whilst the first quarter of the previous year included a deferred tax credit at the South Asia Gateway Terminals (SAGT),” John Keells Holdings Chairman Krishan Balendra said.

Excluding these impacts, group EBITDA for 1Q25 recorded an increase of 2 percent to Rs.8.47 billion.

A stress on the group performance was also the leisure sector due to a decline in profitability in the Maldivian Resorts segment on account of lower occupancy.

Group profit before tax (PBT) at a negative Rs.204 million in the 1Q25 is a decrease over the Rs.1.40 billion recorded in the previous financial year. Group PBT declined on account of a non-cash exchange loss of Rs.1.25 billion on the outstanding US$ 216 million term loan facility at Waterfront Properties Limited (WPL).

Excluding the deferred tax credit at SAGT and the exchange loss at WPL, group PBT increased by 71 percent to Rs.1.05 billion as against Rs.612 million recorded in the same period of the previous year.

In a commentary that followed the release of the 1Q financial results, Balendra noted that the finishing works at the ‘City of Dreams Sri Lanka’ integrated resort is progressing well, with the 687-key ‘Cinnamon Life’ hotel, restaurants and banquet facilities being in the final stages of fit-out to commence operations in October 2024.

The remainder of the project comprising of the 113-key ‘Nuwa’ hotel, gaming operations and retail mall, will be operational, in a phased manner, with overall completion of these elements scheduled for mid-CY2025.

Subsequent to the 20-year lease agreement for the demarcated gaming space at the ‘City of Dreams Sri Lanka’ being executed between WPL and the locally incorporated subsidiary of Melco Resorts & Entertainment Limited (Melco), has mobilised the teams to commence the fit-out work of the gaming space.

The work on the West Container Terminal (WCT-1) at the Port of Colombo is progressing well. The first batch of quay and yard cranes will arrive in August 2024, following which the commissioning and automation is expected to be completed by the third quarter of 2024/25. The first phase of the terminal is slated to be operational in 4Q25.

Profitability at SAGT recorded an increase driven by double-digit growth in throughput, on account of both domestic and transshipment volumes.

The group’s bunkering business, Lanka Marine Services (LMS) recorded double-digit volume growth during the quarter although profitability was impacted due a contraction in margins on account of volatile global fuel oil prices and intensified competition from local and regional players.

Both the beverages and the frozen confectionery businesses recorded an increase in EBITDA driven by a significant growth in margins and volumes.

The leisure industry group EBITDA of negative Rs.794 million in the first quarter of 2024/25 is a decrease over the EBITDA for the first quarter of the previous financial year. Excluding the ‘City of Dreams Sri Lanka’ integrated resort, the leisure industry group EBITDA is a negative Rs.18 million

The supermarket business recorded a strong performance during the quarter, with same store sales recording encouraging growth of 12 percent, driven by customer footfall growth of 12 percent, resulting in growth in profitability and margins. Nations Trust Bank PLC (NTB) recorded a strong growth in profitability aided by loan growth, lower impairments and increased trading and fee income while Union Assurance PLC (UA) recorded double-digit growth in gross written premiums, driven by renewal premiums and regular new business premiums.

The group’s carbon footprint per million rupees of revenue decreased by 3 percent to 0.41 MT, and the water withdrawal per million rupees of revenue decreased by 15 percent to 7.46 cubic metres when compared to the corresponding quarter of the previous year.

The profit attributable to equity holders is a negative Rs.868 million compared to Rs.1.47 billion in the corresponding period of the previous financial year.

22 Nov 2024 52 minute ago

22 Nov 2024 1 hours ago

22 Nov 2024 2 hours ago

22 Nov 2024 3 hours ago

22 Nov 2024 4 hours ago