21 Nov 2024 - {{hitsCtrl.values.hits}}

By First Capital Research

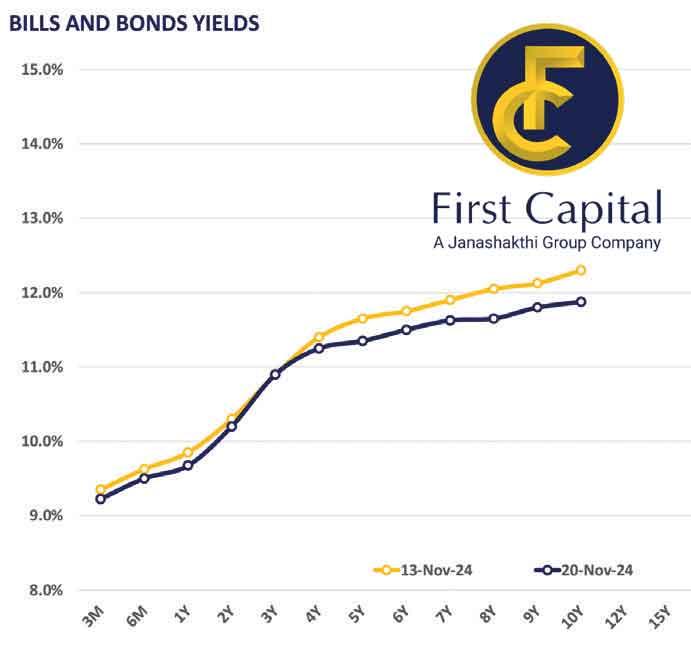

The secondary market yield curve continued to dip across the board, driven by the sustained bullish sentiment, while generating moderate volumes.

Accordingly, buying interest was seen in the 01.08.26 and 15.12.26 maturities, with transactions occurring between 10.30 percent and 10.05 percent. Meanwhile, the 01.05.27, 15.09.27 and 15.12.27 maturities hovered in the range of 11.00 percent to 10.80 percent. Moreover, the mid tenure maturities 15.02.28 and 15.03.28 traded between 11.15 percent-11.10 percent, while, 01.05.28 and 01.07.28 changed hands between 11.25 percent-11.18 percent and the 15.12.28 maturity traded in the range of 11.30 percent-11.25 percent. Moreover, on the long end, 15.06.29 and 15.09.29 hovered between 11.45 percent-11.35 percent while 01.10.32 was also seen actively trading between 11.65 percent-11.60 percent.

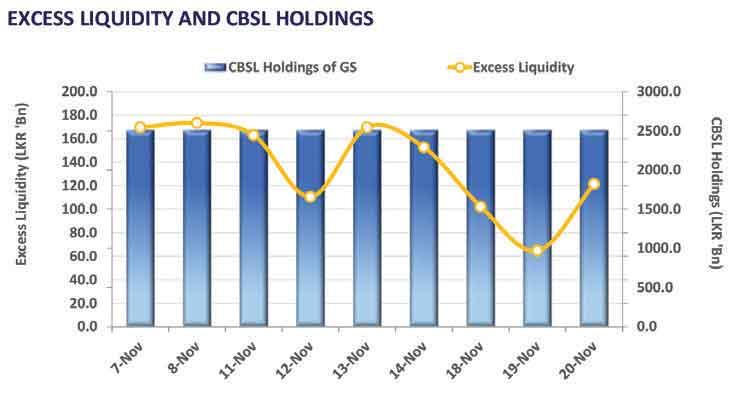

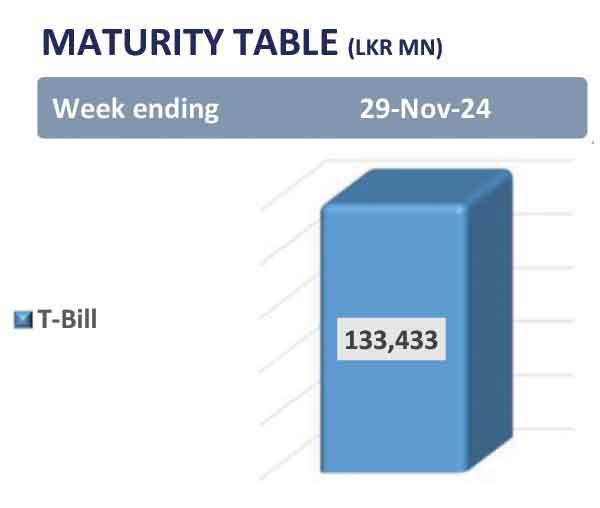

Meanwhile, at yesterday’s weekly T-bill auction, the Central Bank fully accepted the total offered amount of Rs.145.0 billion, with each maturity fully subscribed. Additionally, the six-month T-bills saw a stronger demand, with bids reaching twice the amount offered. Meanwhile, the weighted average rates further dipped across the board for the second consecutive week. Accordingly, the three-month bill declined by 5bps to 9.30 percent, the six-month bill dropped by 4bps to 9.60 percent and the one-year bill declined by 10bps to 9.78 percent. On the external side, the Sri Lankan rupee further appreciated against the greenback, closing at Rs.290.9. Meanwhile, overnight liquidity recorded at Rs.121.4 billion while the Central Bank holdings remained unchanged at Rs.2,515.6 billion.

03 Dec 2024 45 minute ago

03 Dec 2024 2 hours ago

03 Dec 2024 3 hours ago

03 Dec 2024 3 hours ago

03 Dec 2024 5 hours ago