19 Jun 2024 - {{hitsCtrl.values.hits}}

Let us not kid ourselves. The International Monetary Fund (IMF) has nothing to do in Sri Lanka, not least with what Sri Lanka has been going through.

Let us not kid ourselves. The International Monetary Fund (IMF) has nothing to do in Sri Lanka, not least with what Sri Lanka has been going through.

So, you might wonder, if that’s the case, what are they doing here? You are right. They are at the wrong place, invited here by a wrong set of people, whose brains have been programmed to function in only one way, which they think is the only way.

What Sri Lanka was going through wasn’t anything different from what any other country in the world went through in the last couple of years, having to deal with a pandemic, which sent shivers through the global economy in unprecedented scale, unbalancing the supply and demand conditions all over the world.

Already weakened by the economic mismanagement by the good governance regime and accumulating debt in their five-year term by levels far greater than the totality of the amount raised in the preceding decade and also gripped by the higher taxes by the then IMF programme – the 16th one, the Sri Lankan economy could not have been in a worse spot to enter into the pandemic.

What compounded the problems was the war in Ukraine, which sent the global energy, food and other commodities prices spiralling before settling lower from the second half of 2022.

I repeat, it wasn’t the tax cuts, it wasn’t the money printing that caused Sri Lanka’s troubled time. If one says otherwise, they are out of their minds.

Any man who has been closely watching these events unfolding globally and at home would know that still the countries around the world are scrambling to come out of the imbalances left by the pandemic.

This is why the United States and European economies were holding up on the back of the fastest interest rate increases executed to fight the record high inflation there in 2022, proving the recession calls by many economists wrong.

But the majority Sri Lankans were quick to find scapegoats and took to streets. That’s natural. That’s what they do.

And our so-called experts and the self-proclaimed ones, including the Colombo-based know-it-all think tank talking heads, saw the gullibility of the masses, specially the educated middle class, exploited the opportunity and filled air waves in convincing that the IMF was the only solace and somehow managed to put the fox in the henhouse.

They created a non-existent demon, made people afraid of it and said whom to blame for it.

Let us also be abundantly clear. It wasn’t the Central Bank that brought inflation down. The IMF didn’t bail out Sri Lanka and President Wickramasinghe didn’t fix the economy.

Instead, all three, wittingly or unwittingly, made matters worse, deepened and prolonged the economic troubles, which could have well been a short-term one.

So, why do I say why we need to end the current IMF nonsense forthwith?

First, Sri Lanka does not have a debt crisis

This might strike you hard, as the drumbeat you hear day-in-and-day-out is to the contrary, don’t you? Yes. But the truth is Sri Lanka doesn’t have a debt crisis. It temporarily had a harder time serving its debt because its major foreign currency inflows were either slowed down or some of which nearly came to a halt due to the pandemic.

The nearly US $ 5.0 billion annual tourism income was just one.

Debt’s sustainability is not measured by its size or magnitude. It is measured by your ability to service it or whether you generate sufficient cash flows to service it.

Of course, this ability weakened since 2020 because of the aforementioned reasons. Of course, it could happen to anybody; an individual, a company and a country is of no difference. That depends on what you do with the money you borrowed, the economic cycles and of course, black swans like pandemics, the latter two of which you hardly have any control over.

But that doesn’t mean that Sri Lanka should default. Would it have been better to strive harder to maintain the country’s impeccable track record by doing all it can to address it or would you make a mountain out of a molehill and make a pronouncement of a default?

Sri Lanka was looking at stop-gap measures until we ride out the extremely tough time, before the new and current authorities, who took the helm at the Central Bank and Treasury Department, announced a debt standstill, a nicer term to a ‘default’.

And that was all they knew for what they have been trained all their lives as economists.

Economists typically get dreaded at the sheer magnitude of debt and start trembling not knowing what to do. Many economists and others do not understand debt.

But those who know what debt is, what it could do and who have been going through repeated economic cycles with high debt piles on their shoulders, are less worried and wouldn’t call it the end of the world.

Although it is easier said than done, when the push comes to shove, they make it a priority to manage the cash flow until the situations turn less severe.

Sri Lankans didn’t have the patience till that was done and hence, turned what could well have been temporary hardships into a prolonged economic crisis and exported its economic management to a Washington-based institute, which has no clue of what it takes to tick the Sri Lankan economy.

In the process, you got your interest rates, taxes and utility tariffs up to the hilt, lost your economic autonomy and are losing your public assets, citing massive losses, including and funny enough Sri Lanka Cashew Corporation got some foreigners to interfere into upending how you run your Central Bank and government.

We are back in the pre-pandemic era. No more new normals as many pundits and corporate chieftains said giving speeches back then on Zoom. We can now start repaying debt, restructured or otherwise. What you need to do is just look at the cash flows.

The IMF last week said, “Nevertheless, the economy is still vulnerable and the path to debt sustainability remains knife-edged,” after two years from staying with its programme. So, its programme hasn’t worked and never will.

So, if we don’t have a debt crisis, the pre-eminent reason why we got them down here, it’s high time we called it quits.

Taxes are killing this economy

The cornerstone of any IMF programme is to raise government revenues, cut deficit no matter what circumstance you are in, end subsidies, cut spending, market-price energy, utilities and all other state services and to ensure they achieve what they are set out to achieve when the IMF was set up and funded by their masters in the West.

Well, one could say these reforms are necessary to fix the economy, also to ensure the IMF sees its money back.

On the latter, it might want to see its money back but I doubt just US $ 2.9 billion could make much of a difference, even if it didn’t get it back. Look at the hundreds of billions of dollars the IMF lends and US government prints with its eyes closed to send to a war fought by a former comedian in Eastern Europe.

On the former, let me delve into that on another day because this space isn’t nearly enough for that debate.

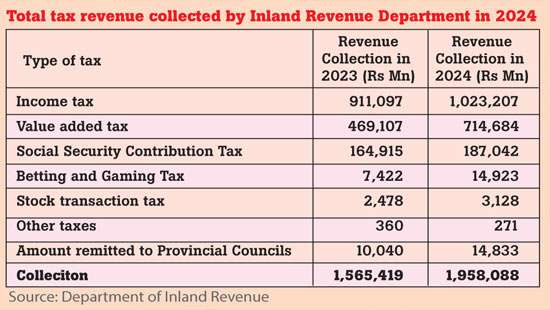

Make no mistake; the taxes at these levels are killing the economy and those are what holding the economy back, despite the interest rates falling back to single-digit levels.

The IMF’s obsession with taxes and its relentless pursuit of getting new and more taxes imposed were abundantly clear from its statement released just last week, soon after approving its second programme review.

This was when Sri Lanka was outperforming its budget in revenues, thanks to the increase in the Value Added Tax (VAT) and cutting the VAT-free threshold.

They appear to have now become unstoppable, wanting more taxes, including tax on incomes, which do not even exist. They have been fighting hard for an imposition of a wealth tax, which does not even exist in the United States.

They also want to end the VAT exemptions on services exports and charge VAT on digital services – the two insidious ways of preventing Sri Lanka from growing its services exports and building a digital economy.

Under the current IMF deal, Sri Lanka now taxes exporters at the same general Corporate Income Tax rate and so does it on the agricultural sector and small businesses.

Here is a country that is literally crying for dollar incomes, wanting so badly to nurture and strengthen exporters and foster entrepreneurship. But at policymaking level, there is no shortage of supreme idiocy to kill them from within.

Sri Lanka cannot grow without government loosening purse strings

We have heard that the private sector is the engine of growth but it was state spending that actually has driven the growth in the Sri Lankan economy, including creating opportunities for the private sector.

Unlike in the West, in Sri Lanka, the private sector has hardly been big capital spenders.

The government has almost always led the charge in driving growth by its spending. Look at the post-war development that recorded the highest ever average annual growth recorded by Sri Lanka.

While fiscal profligacy must not be condoned, you have to get your government to loosen its purse strings and put that money to work.

With the IMF and its tough fiscal deficit targets, the government cannot put its money back to work, even to areas that deem extremely necessary for development and growth.

And the funny thing is that Sri Lanka’s economy is run by a bunch of foreigners wearing pinstripe suits, as they decide what is good for Sri Lanka. Its many finance ministers are reduced to mere messengers, as they follow where the IMF goes and one such minister is quick to take to Twitter (now X) to say what they said or they might have said.

Its Treasury secretary is very obedient in following through on what the IMF says and so does appear the Central Bank chief, although he pretends he is less so.

New Central Bank Act impedes growth

Making matters even worse, the new Central Bank Act, which was brought at the behest of the IMF, prevented the institute from helping the government from the moneys it needs, when it needs, unless it is defined as an emergency. But the adjudicator of what an emergency is taken away from the government, as it appears and has rested with the Central Bank and IMF, two unelected sets of bureaucrats.

How stupid is it to let such crucial decisions to be taken by unelected bureaucrats?

While the full independence of the Central Bank looks good on paper, a monetary policy, which is fully divorced from the fiscal policy and direction of the government may not entirely be a good recipe for Sri Lanka due to many reasons.

IMF’s overreach on internal affairs

The IMF from the beginning was interfering unduly in the internal affairs of the government and even conducted what it called the Governance Diagnostic Assessment, in which it looked at multiple areas targeting corruption vulnerabilities and governance weakness, for which it came up with a 16-point plan as its recommendation.

While it says this was conducted at the request of the Sri Lankan authorities, either because the local authorities think the IMF could do such an assessment better than them or they are in fact dumber that they cannot get their heads around their own governance system, such exercises tantamount to overreach by the IMF, which should not have been allowed in the first place.

SOE reforms do not mean fire sale

While President Wickremesinghe is infamous for selling national assets, people of this country cannot suddenly wake up to a day where all your national assets are gone.

They are there for a reason and they serve their purpose even at times when they were making losses. Let us not forget the CPC and CEB losses at times are profits in your income statement. Difficult to understand? Think.

Dealing with their endless losses and endemic inefficiencies is a different matter but selling them outright is not an excuse.

There are many ways to deal with their financial losses and inefficiencies, while keeping them at state ownership.

If the IMF is not happy and they insist only on selling them off as the only form of SOE reforms, may our leaders have the courage to ask them to ‘go’, because you are going to miss them when they are gone.

Local and foreign investors unenthusiastic about IMF and its money anymore

If you look at the response of the investors to the news of the IMF approving the second programme review last week and the immediate access to the third programme tranche, it didn’t cheer them at all.

In fact, they shrugged it off and sent the stocks down, not just one but three days in a row.

They finally appear to have come to the realisation that US $ 330 million coming now and then, is nothing compared to what we can generate by rebuilding the economy within through exports, tourism and investments. And remittances have been robust.

And they also think the taxes are taking away much of the juice out of their returns, as they hit harder on the top and bottom lines of the companies they invest in and thus, it isn’t worth the pain of remaining in the programme.

Show the IMF the door and cut taxes, both direct and indirect, to bring back animal spirits into all markets.

They are robbing your money and economic well-being

By taxing at these levels and mulling more new taxes, you effectively transfer the resources from the pocketbooks of the people and businesses, back to the government coffers.

Governments anywhere are no efficient allocators of resources.

The money is better used when they are left with the people and businesses, as they decide where to spend and when to spend based on their economic self-interests.

Further, at these levels of taxes, Sri Lanka is unlikely to exceed more than 3 to 4 percent growth in its economy in the medium term, the level of which is nearly not sufficient to put the money back in the hands of the people to reclaim the lost purchasing power in the last couple of years and then to have them the economic well-being they aspire.

Sri Lanka’s lost decade from 2015 to 2024 is impossible to be undone unless policies are brought to unleash the animal spirits of the economy to a high single-digit growth consistently in the next 10 years.

For it to happen, you need people who are bold enough to ask the IMF to leave.

(Dilina Kulathunga can be reached at [email protected])

06 Jan 2025 25 minute ago

06 Jan 2025 1 hours ago

06 Jan 2025 1 hours ago

06 Jan 2025 1 hours ago

06 Jan 2025 1 hours ago