24 Jul 2024 - {{hitsCtrl.values.hits}}

By First Capital Research

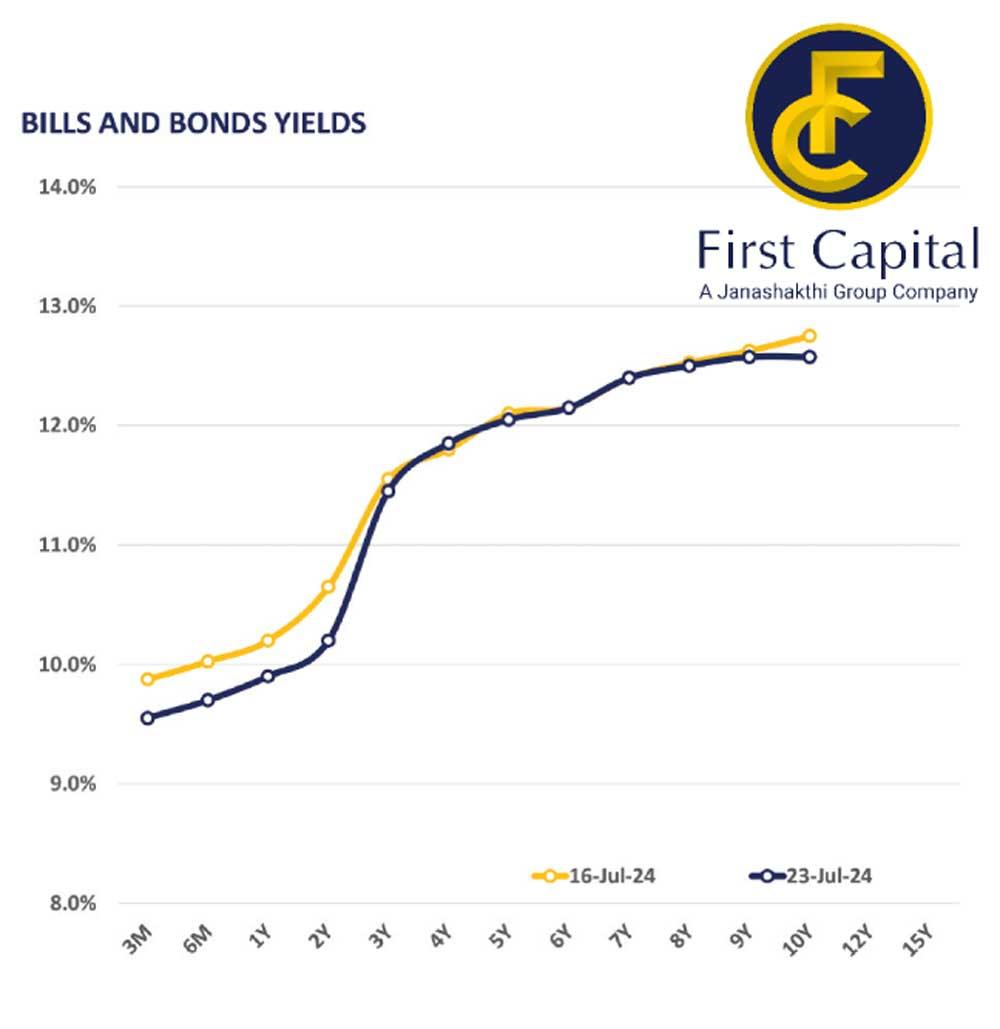

The secondary market yield curve remained broadly unchanged yesterday amidst limited activities and low trading volumes across the market, ahead of today’s monetary policy decision and bill auction.

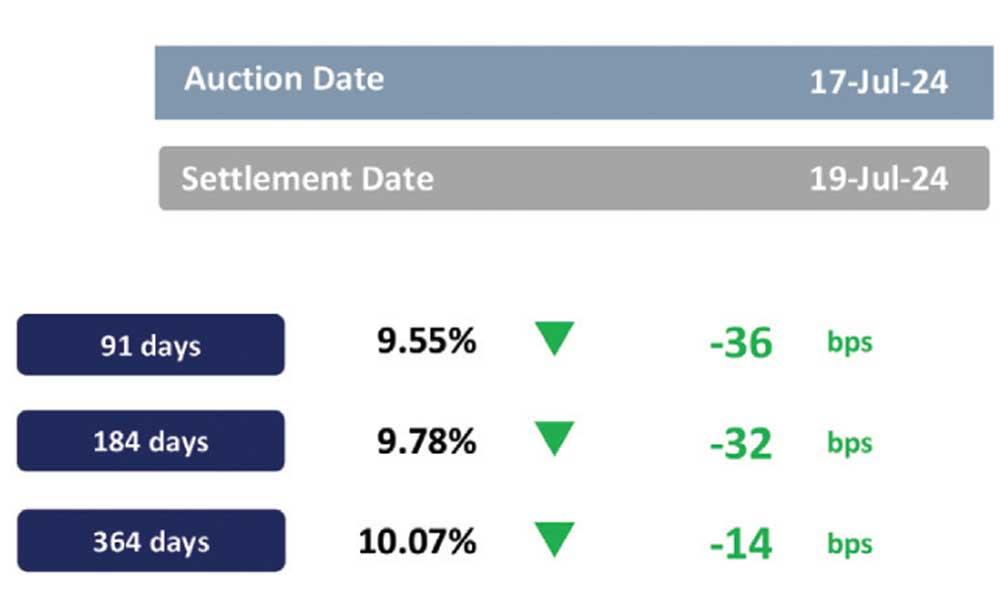

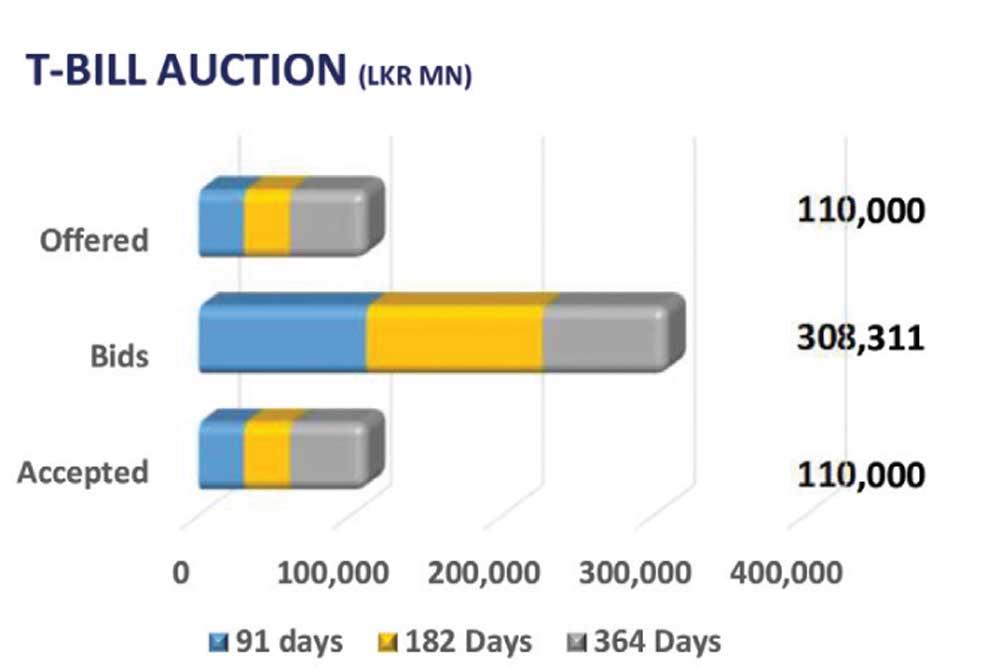

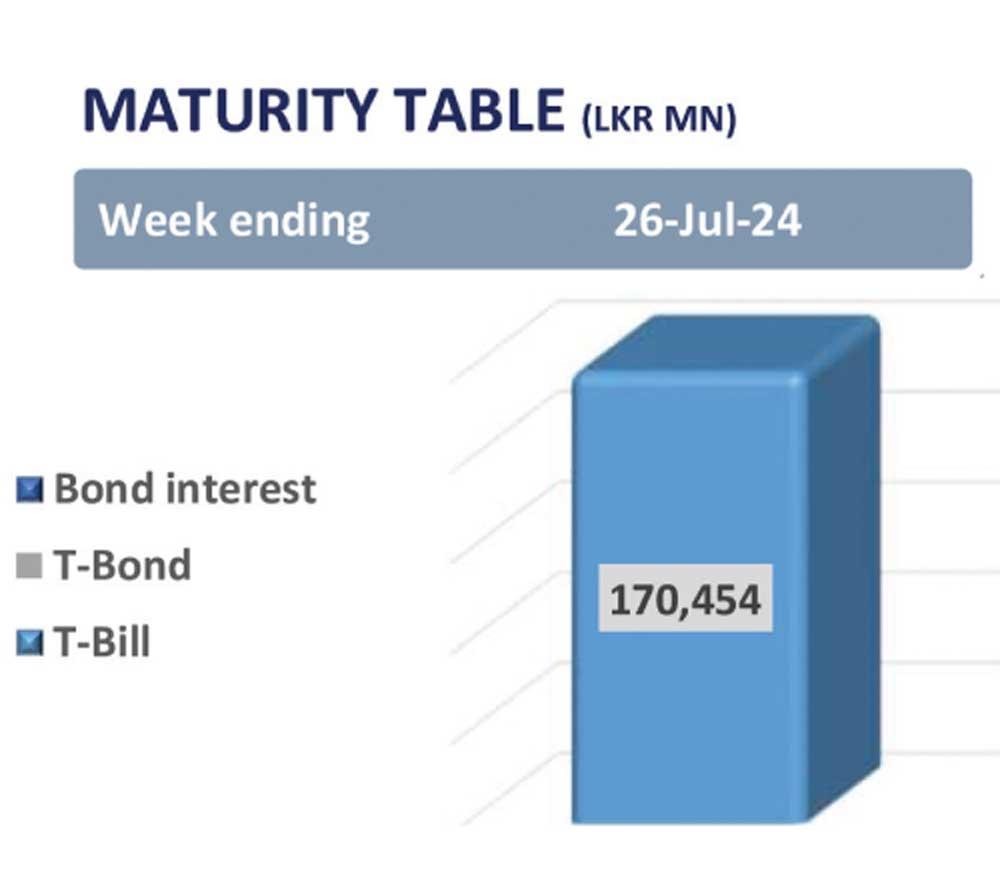

Investors opted for a wait and see approach in anticipation of policy rate changes, and the results of the T-bill auction to be held today. At today’s weekly T-bill auction, CBSL is expected to raise Rs. 160.0bn through the issuance of Rs. 45.0bn from the 91-day maturity, Rs. 45.0bn is expected to be raised from the 182-day maturity, while Rs. 70.0bn is expected to be raised from the 364-day maturity.

Among the traded maturities, notable trades were amongst mid tenors, primarily the 2028 maturities, where 15.03.28, 01.05.28, 01.07.28, 01.09.28, and 15.09.29 were seen trading at rates of 11.75%, 11.82%, 11.80%, 11.95%, and 12.05% respectively. Meanwhile, on the long end of the curve, 01.12.31 was seen trading at a rate of 12.42%.

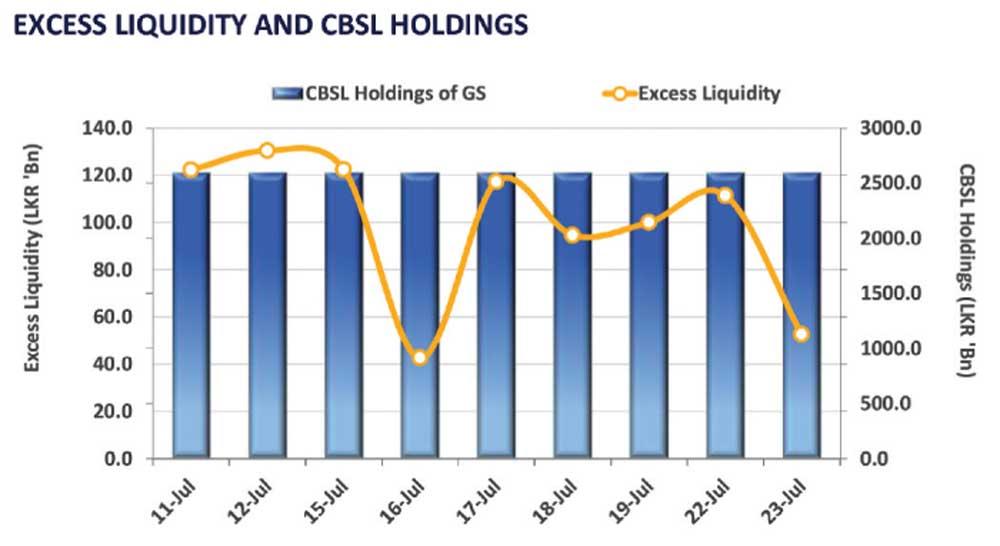

On the external front, LKR depreciated slightly against USD, closing at 303.72/USD compared to 303.69/USD recorded the previous day. Meanwhile, CBSL Holdings of government securities remained unchanged at Rs. 2,595.6bn yesterday. Overnight liquidity in the banking system contracted to Rs. 52.63bn from Rs. 111.43bn recorded the previous day.

26 Nov 2024 2 hours ago

26 Nov 2024 2 hours ago

26 Nov 2024 2 hours ago

26 Nov 2024 3 hours ago

26 Nov 2024 4 hours ago