BY A.A. Thilakarathne

Former Finance Minister Ravi Karunanayake in his budget speech for 2017 stated that the tax system of the country is revisited with emphasis being made on the creation of a much simpler tax regime with minimum tax exemptions and a broadened tax base.

He also said that the capital gains tax (CGT) would be introduced with effect from April 1, 2017, at the rate of 10 percent, because they consider this tax to be equitable as it bridges the income gap and assists the government initiatives in poverty alleviation. Therefore, it is very clear the CGT has been introduced to achieve mainly two objectives.

He also mentioned in his budget speech that the government intends to increase the direct tax component to 40 percent from around 20 percent at present and gradually reduce the indirect taxes to 60 percent from around 80 percent in the medium term. Thus, a commendable step is taken in the right direction at this belated stage to reintroduce the CGT, which was abolished by the then United National Party (UNP) in power in the year 2002.

Accordingly, the new Inland Revenue Act has imposed a CGT on the gain from the realization of an asset with effect from April 1, 2018. This article attempts to see some implications and the impact of the CGT in its implementation.

What is meant by capital gains tax?

In a business, land, buildings, equipment, inventory and raw materials as well as stocks, bonds and cash deposits are considered as capital. An individual’s capital includes real estate that has a cash value and financial assets, such as bank deposits. Accordingly, the gains earned out of capital are called capital gains.

Taxation of capital has been a feature of the Sri Lankan tax system for several years and has taken many forms. Taxes on immovable property were levied in the form of a land tax between 1960 and 1962. Immovable property was also included in the once and for all capital levy in 1971.

Estate duty was an old tax since 1919 and it was abolished in the year 1985. Taxation on capital gains was introduced as part of the Kaldor Reforms in 1957 and it lasted until the year in 2002.

Stamp duty too is charged on the consideration value of the transfer, gift or exchange of immovable properties as well as on the execution of some instruments in terms of the Stamp Duty Act No.43 of 1982. Therefore, stamp duty also can be treated as a tax charged in relation to capital asset and stamp duty goes hand in hand with the capital gains.

Why capital gains tax is introduced?

Gross domestic product (GDP) of Sri Lanka was US $ 67.18 billion in 2013 and its per capita income remained at US $ 3280 in 2013. The tax revenue to GDP remained low at 13.6 percent in 2013 and it played a major role in the government revenue as well.

Likewise, a properly administered tax regime is indispensible for the economic well-being of an organised state. When analysing the data of the Inland Revenue Department, it was evident by the statistics in recent time that the tax revenue as a percentage of GDP has been on remarkable decline over a long period of time.

This situation leads to a serious concern for the authorities responsible and accountable for economic management and development of the country. An attempt is made to examine the key elements of the capital gains regime in order to determine its impact on the Sri Lankan current tax system.

The research was done primarily by using secondary data, with a view to evaluating the CGT procedures as well as various aspects of the CGT in its implementation.

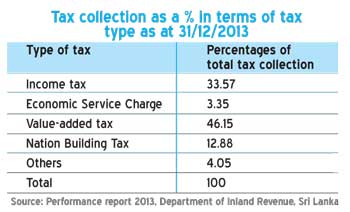

The government revenue mainly consists of tax revenue and non-tax revenue. Tax revenue consists of several taxes such as income tax (IT), value-added tax (VAT), Nation Building Tax (NBT) and Economic Service Charge (ESC), etc. which are presently administered in Sri Lanka and they bring a larger share to the government revenue. The taxes and their contribution to the total tax revenue are as stated in the table.

When the CGT was in force, it amounted to a 1.1 percent of the total tax collection in the said year, according to the administration report 1997 published by the Inland Revenue Department. It should be noted that the CGT was abolished in the year 2002 and it was not liable to be taxed as a source of income for a period of 16 years in the country.

Tax revenue/GDP ratio

In the year 2013, the total tax revenue was Rs.1006 billion and it represented 51.69 percent of the total government revenue. Its contribution to GDP stood at 11.59 percent. However, the proportion of tax revenue to GDP in other countries in the world is very much higher when it is compared to Sri Lanka.

According to the Organisation for Economic Cooperation and Development (OECD) complete database, the tax revenue as a percentage of GDP in Australia was 30.8 percent (2012), Norway 43.6 percent and Denmark 49 percent. This ratio in the developing countries such as India was 17.7 percent, Malaysia 15.5 percent and the Maldives 12.5 percent. In the year 2012, Sri Lanka was 15.3 percent and the government projected to increase the tax/GDP ratio to 19.0 percent by the year 2016. But it was not achieved as projected.

Economists argue that for a country to become developed, it should collect taxes at a ratio of 20-30 percent of GDP. In order to maintain the present economic growth rate at 8 percent and to reduce the government debt/GDP ratio (82 percent), it is the responsibility of the government to increase the tax/GDP ratio up to a projected level. In this sense, the tax revenue in Sri Lanka plays a vital role and broadening tax base also becomes equally important in today’s context.

Rationale for taxing capital gains

The case for taxing capital gains rests on the premise that the capital gains provide the recipient with just as much economic power over goods and services as any other form of income. If the capital gains are not taxed as income, certain individuals and groups will receive preferential treatment relative to others who have the same ability to pay and undermine the progressivity of the tax system.

The taxation of capital gains prevents the misallocation of resources and minimizes the opportunities for tax avoidance. In other words, the CGT will help to decrease the unfairly distribution of income to a certain extent. For example, in the case of increase of the Port and Air Port Levy (PAL), excise duty, NBT, VAT, the prices of consumer goods will go up and affect the poorest of the poor rather than the affluent.

Generally transactions relating to land, building, membership interest in a company and other financial assets are taking place among those who have. In that context, the CGT is comparatively a better source of income for the state coffers rather than increasing the PAL, NBT, VAT and excise duty, which will lead to increase the prices of consumer goods.

CGT under old Inland Revenue Acts

From the year 1957, the CGT has been in existence under various acts of the country. The CGT was imposed under Section 7 of the Inland Revenue Act No. 38 of 2000 and it lasted until the year 2002.

Capital gains arise from change of ownership of any property and from gains arising from certain transactions such as surrender or relinquishment of any right in any property, thereby immovable property as well as the moveable property were subject to be liable for the CGT.

The formation of a company, dissolution of a company and amalgamation or merger of two or more businesses or companies were liable for the CGT. At the same time, there were some exemptions for such gains under Section 14 of the said acts.

Under the earlier acts, the rate of the CGT was depending on the period of ownership held by the owner. The shorter the period of ownership held by the owner, higher the rate of tax. It varied depending on the period of ownership.

- Period of ownership of property between two to five years – 20 percent

- Period of ownership between five to 15 years – 17.5 percent

- Period of ownership between 15 to 20 years – 12.5 percent

- Period of ownership between 20 to 25 years – 5 percent

- Period of ownership of property held in possession for more than 25 years – exempt

- Period of time less than two years was treated as a trading income and it was taxed at normal tax rates. There were several tax exemptions under the old Inland Revenue Acts and such exemptions have not been taken into consideration when drafting the new act.

CGT under new Inland Revenue Act

Section 36 to Section 50 of the new Inland Revenue Act provides the manner in which the capital gain is arisen and how it becomes liable to tax.

Section 36 of the act provides that capital gains arise from the realization of an asset or the sum of the consideration received or receivable for the asset or liability exceeds the cost of the asset or liability at the time of realization. In other words, capital gain will be the result of sale price less the price of purchase.

In addition, expenditures on advertising, transfer taxes, stamp duties, charges imposed by local authorities will be allowed to be deducted from the capital gain. The net difference between the sale price and purchase price will be treated as net capital gain. Accordingly, in calculating the CGT, the definition of capital assets, cost of assets, realization of assets and consideration will be very important.

The cost of the asset will be allowed to deduct from the price of purchase. In terms of Section 37(1), the cost of the asset includes the expenditure incurred in acquiring the asset such as construction, manufacture or production of the asset and expenditure on altering, improving, maintaining or repairing the asset.

Incidental expenditure in acquiring and realizing an asset, such as advertising expenditure, transfer taxes and other levies paid to local authorities, expenditure of establishing, preserving or defending ownership of the asset will be allowed as deduction from the purchase price. Expenditure on improvements, fencing, repairing the asset and remunerations paid for services such as accountant, agent and auctioneer can be deducted.

Realization means a person parts with the ownership of the asset, including when the asset is sold, exchanged, transferred, distributed, cancelled, redeemed, destroyed, lost, expired, expropriated or surrendered.

Exemptions

The trading stock or depreciable assets are not treated as realization of an asset. When an asset is realized due to a death of a person, it will not be included in the realization of an asset. Transfer of an asset from husband to his spouse in a bona fide separation is not treated as realization of asset and the CGT will not arise.

When a transfer of an asset takes place due to death of a person, the CGT will not arise. Realization of trading stock, depreciable assets, investment assets or capital assets of a business will not be fallen into the source of the CGT. There are few other items which have been made exempted from the CGT. Consideration received for an asset shall not include an exempt amount, a final with holding payment or trading stock.

Consideration means the value received for an asset of a person at a particular time shall be amounts received or receivable by the person for the asset including the fair market value of any consideration in kind determined at the time of realization.

Rate of CGT

Under the new Inland Revenue Act, the CGT is taxed at a flat rate of 10 percent, irrespective of the period of ownership held by the owner of the asset.

Registration of transfer of capital assets

Under Clause 50 of the Inland Revenue Bill, any person authorized by law to accept, register or approve the transfer of a capital asset shall not register the same unless he is satisfied that any tax payable under this act has been paid. At the committee stage, the said clause has been amended as, “The manner and the procedure relating to the payment of tax on the gain from realization of an asset may be specified by the Commissioner General.”

Accordingly, when registering a document for transfer of properties, it should be ensured that the CGT thereon has been paid or not. The Commissioner General of Inland Revenue is supposed to prepare a procedure in this regard.

Stamp duty

Stamp duty is imposed on the instruments relating to transfer of movable and immovable properties and on the registration of documents. Stamp duty and the CGT should be paid based on the same transaction on deferent basis.

Stamp duty is charged and collected in terms of the provisions of Stamp Duty Act No.43 of 1982. Stamp duty was repealed by the Finance Act No.11 of 2002 and it was reintroduced by the Stamp Duty Act (Special Provisions) Act No.12 of 2006.

Accordingly, the instruments relating to transfer of properties should be stamped on the rates published by gazette notifications. Anyway, the stamp duty so imposed and collected by the central government should be transferred to the Provincial Council in terms of Section 2 of the Provincial Councils (Transfer of Stamp Duty) Act No.13 of 2011.

Conclusion

The newly introduced CGT is not complicated and it has only one flat rate of 10 percent. The CGT will broaden the tax base and it will bring a considerable income to the state coffers while the CGT helps to ease unequal distribution of income. It will help to increase direct tax ratio to a certain extent in the long run.

The exempt items should be clearly distinguished in the procedure and simpler procedures should be adopted in order to enable the tax payer to distinguish exempt items clearly and to ensure that the taxpayer does not face many complications.

The CGT will not be a panacea for all the diseases but it will be a solace for the prevailing tax system if properly administered by the relevant authorities and if not it will not be a Saradiyel’s budget.

(A.A. Thilakarathne, an Attorney-at-Law, is former Assistant Commissioner of Inland Revenue)