03 Nov 2016 - {{hitsCtrl.values.hits}}

Sri Lanka’s public finances are at a perilous state. Already weakened by years of low revenue growth and high external debt to fund a public investment-led growth process, systemic weaknesses coalesced in 2015 to put the country on the cusp of falling into a public debt-triggered economic crisis. A ballooning fiscal deficit and excessive public debt accumulation have resulted in a rising debt service burden; the conduct of the monetary policy and exchange rate management has been compromised in attempts to deal with the fallout of funding the fiscal deficit gap.

Therefore, fiscal policy reforms are urgently required to avert an impending economic crisis. At the outset, public expenditure needs to be rationalized by diverting resources away from loss-making public entities and towards investments with high economic returns. Simultaneously, the government’s revenue mobilizing framework should be re-evaluated in view of broadening the revenue base and maximizing revenue potential. Only fundamental reforms to public finances will guarantee a measure of macroeconomic stability and improved growth outlook.

Therefore, fiscal policy reforms are urgently required to avert an impending economic crisis. At the outset, public expenditure needs to be rationalized by diverting resources away from loss-making public entities and towards investments with high economic returns. Simultaneously, the government’s revenue mobilizing framework should be re-evaluated in view of broadening the revenue base and maximizing revenue potential. Only fundamental reforms to public finances will guarantee a measure of macroeconomic stability and improved growth outlook.

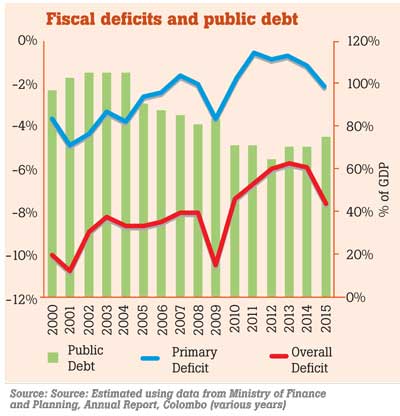

Successive Sri Lankan governments since independence have accumulated unsustainable fiscal deficits due to a combination of populist expenditure projects and low revenue streams. Despite some improvements, deficits have continued to average 7-8 percent of gross domestic product (GDP) with knock-on effects on other critical areas of macroeconomic policy management, most notably fuelling high and volatile rates of inflation. With rising fiscal imbalances, the country’s indebtedness also rose – peaking most recently at 105 percent of GDP in 2002 – narrowing the options for policy manoeuvrability and limiting the ability to respond appropriately to domestic and external shocks.

Successive Sri Lankan governments since independence have accumulated unsustainable fiscal deficits due to a combination of populist expenditure projects and low revenue streams. Despite some improvements, deficits have continued to average 7-8 percent of gross domestic product (GDP) with knock-on effects on other critical areas of macroeconomic policy management, most notably fuelling high and volatile rates of inflation. With rising fiscal imbalances, the country’s indebtedness also rose – peaking most recently at 105 percent of GDP in 2002 – narrowing the options for policy manoeuvrability and limiting the ability to respond appropriately to domestic and external shocks.

Since 2009, Sri Lanka appears at first glance to have made some headway in reversing the country’s fiscal fortunes. The fiscal deficit fell progressively to 5.4 percent of GDP in 2013, while the public debt-to-GDP ratio too climbed down steadily to around 70 percent of GDP. However, the explanation for this lies in more robust nominal GDP growth over the same period than any underlying efforts at addressing structural weaknesses in fiscal policy management.

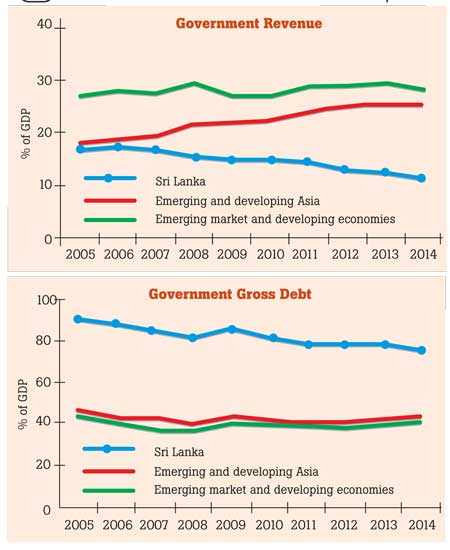

The government revenue generation is well below the desired level, while the government debt burden is much higher than countries at similar levels of development.

Government revenue

The bulk of Sri Lanka’s tax revenue is sourced through indirect taxes, followed by direct taxes and non-tax revenue. A value-added tax (VAT) and a nation building tax (NBT) are the main contributors of indirect tax revenue. Whilst the share of direct taxes has remained more or less unchanged over the years, revenue from indirect taxation and non-tax sources have declined significantly from a high of 5.9 percent of GDP in 2004 to a historic low of 2.6 percent of GDP in 2015. Consequently, revenue as a share of GDP has declined persistently from around 17 percent in 2000 to a historic low of 11.5 percent in 2014. Alarmingly, this is despite a steady rise in per capita income in the country over the same period. In response, governments have resorted to offset the decline in indirect tax revenue through an increase in trade taxes. These policies have thus negatively affected the trade and investment productivity of the country. These unsustainable practices continue despite a slew of recommendations made by a Presidential Tax Commission made in 2010.

Expenditure

The composition of current expenditures – primarily made up of salaries and wages, interest payments on public debt and transfers and subsidies – has hardly changed either, underlying the lack of meaningful reform efforts in public finance management. Sri Lanka has a large and growing cadre of public sector employees, estimated to account for approximately 15 percent of the total employed in 2015. Aside from the heavy fiscal recurrent expenditure burden of salaries and a non-funded public sector pension scheme, the Treasury must also grapple with transfers to loss-making state-owned enterprises (SOEs).

The unsustainable financing strategy has been worsened through the extension of government Treasury guarantees, which has effectively increased government liabilities and thereby creates knock-on effects on the profitability of other state institutions and enterprises.

Contrastingly, funding for critical areas such as education and health as a percentage of GDP has declined. Adequate investments in health and education are important not only to ensure a skilled and productive workforce but also to meet broader objectives of socioeconomic development and equity. Furthermore, evidence suggests that although education and health services are provided free of user fees, households on average spend 6.2 percent of their monthly expenditure on health and education, leading to widening inequality.

Public investment

Sri Lanka’s public investment lagged behind for years due to other expenditure priorities, especially defence spending during the conflict. The post-conflict growth agenda saw a renewed focus on public investment, albeit financed mostly through external borrowings. The negative impacts of debt-financed investments are somewhat ameliorated with pertinent investments in projects that produce high returns in dollars (or other exchange) through direct or indirect means. Such returns would better facilitate the repayment of debts. However, politically motivated investments with low returns have resulted in the necessity for debt rollovers and an increasingly expanding debt service burden.

Areas for reform

The legacy of Sri Lanka’s welfare-state, history of populist public spending programmes, poorly managed SOEs and a bloated public sector bureaucracy have made rationalization of expenditures an uphill task. If performance of public finance management on the expenditure front has been mixed, fiscal performance on the revenue front has clearly been very poor since the early 1990s.

The fiscal landscape – marked by high deficits and government borrowing – leaves little leeway to reorient public investment toward high return, high productivity sectors such as education and healthcare. Some degree of expenditure rationalization is necessary, particularly with regard to the loss-making SOEs, poorly targeted subsidies and transfers and populist spending measures adopted from time to time. Therefore, much will depend on the political will to reform.

In the near term, the solution lies squarely in reversing the progressive decline in Sri Lanka’s revenue collection efforts. The widespread and ad hoc use of tax incentives as a tool to entice investments has led to a severe erosion of the tax base. This has also contributed to increasing the complexity of the tax structure, leading to issues of monitoring and compliance. Sri Lanka must urgently re-evaluate this policy stance in view of broadening the tax base and rationalizing the tax structure with the broad aim of simplifying revenue administration and increasing compliance.

Another critical area of intervention that needs attention is to address distributional weaknesses of the current tax system. Historically, Sri Lanka’s tax structure has been a regressive one, with the bulk of revenue generated through production taxes. Whilst the government expressed its intention to arrest this trend and make the structure more progressive, a number of recent tax policy changes introduced in 2016 work counter to this stated objective. With limited fiscal resources constraining investments in social sectors such as health and education and gaps in fiscal support for social protection, especially of the more vulnerable such as the elderly, regressive tax structures will further undermine efforts towards equitable growth and development in the country.

(This policy insight is based on the comprehensive chapter on ‘Fiscal policy for growth: Sustainable financing for development’ in the ‘Sri Lanka: State of the Economy 2016 Report’ - the flagship publication of the Institute of Policy Studies of Sri Lanka (IPS). The complete report can be purchased from the publications section of the IPS, located at No: 100/20, Independence Avenue, Colombo 7)

25 Nov 2024 2 hours ago

25 Nov 2024 3 hours ago

25 Nov 2024 3 hours ago

25 Nov 2024 5 hours ago

25 Nov 2024 5 hours ago