09 May 2017 - {{hitsCtrl.values.hits}}

Asia’s high economic growth rates and huge infrastructure demand, which the recent ADB report Meeting Asia’s Infrastructure Needs estimated at US $ 26 trillion until 2030, offers immense potential for increased private sector participation in infrastructure projects.

Asia’s high economic growth rates and huge infrastructure demand, which the recent ADB report Meeting Asia’s Infrastructure Needs estimated at US $ 26 trillion until 2030, offers immense potential for increased private sector participation in infrastructure projects.

Large banks in developed economies have traditionally been the major financiers of infrastructure projects in emerging economies. However, banks with short-term liabilities are not well suited to hold long-term infrastructure assets on their balance sheets.

Furthermore, revenues from infrastructure projects are generated in local currency, while foreign banks lend in foreign currency. This situation results in the maturity and currency “double mismatch” problem that contributed to the 1997-98 Asian financial crisis.

Against this backdrop, local currency bonds can serve as an alternative avenue for infrastructure financing in Asia and the Pacific. Bonds are an ideal tool for financing long-term infrastructure projects and can thus help to fill the region’s infrastructure investment gap.

This was the rationale behind the creation of the Asian Bond Markets Initiative, launched in 2003 to develop local currency bond markets as an alternative to foreign currency-denominated, short-term bank loans for long-term investment financing.

Bonds also provide suitable investment products for institutional investors with long-term liabilities—such as pension funds and insurers. Many of these are looking to take advantage of currently low interest rates to expand their infrastructure investments.

The emergence of more institutional investors in Asia will further spur the development of infrastructure bond markets.

Credit enhancement lessons from Europe

Although local currency bond financing can help plug financing gaps for long-term infrastructure projects in developing Asia, the region’s infrastructure bond market is still at a nascent stage in terms of issuance relative to the high level of investment required.

There are several factors that make local currency bond financing difficult for infrastructure projects in developing Asia.

First, infrastructure projects tend to be complicated, and require highly specialized expertise from both governments and investors. Second, some risks inherent to these projects cannot be controlled, including political, regulatory, technological and macroeconomic risks. Third, the lack of depth and liquidity of domestic local currency bond markets makes bond financing difficult.

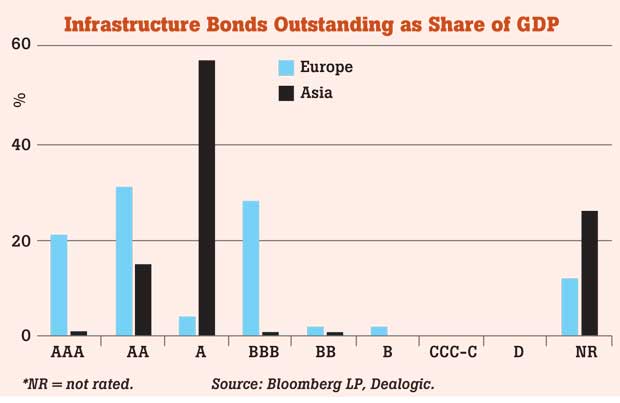

The EU’s Project Bond Initiative (PBI) offers some valuable lessons for developing Asia. Infrastructure bond markets are better developed in the EU, where they amount to 11.7 percent of gross domestic product (GDP), compared to just 6.8 percent in Asia. Credit rating gaps in Asia are one possible explanation for this shortfall.

According to ratings by the three international credit rating agencies, the share of infrastructure bonds rated AA or above is about 52 percent in the EU, but only around 16 percent in Asia. About 57 percent of infrastructure bonds in Asia have an A rating. Infrastructure bonds rated BBB- (investment grade) are frequently issued to finance infrastructure projects in the EU.

Infrastructure bonds pose a challenge for corporate issuers because their credit ratings are lower than those of governments. This raises the cost of debt financing.

Policies that offer preferential treatment for Asian local currency bonds through credit enhancement can be effective way to bridge the ratings gap.

One illuminating example is the European Investment Bank’s Project Bonds Credit Enhancement initiative, which boosts the credit ratings of infrastructure bonds and thus decreases funding costs.

Time for Asian infrastructure bond market development is now

The positive impact of the PBI on the development of EU infrastructure bond markets suggests that ASEAN+3 economies should take policy measures to facilitate the issuance of infrastructure bonds and strengthen the role of the Credit Guarantee and Investment Facility (CGIF) in providing guarantees for infrastructure bonds.

The low credit ratings of Asian infrastructure bonds further strengthen the case for such measures.

Integration of regional bond markets would also help. Infrastructure bond market development is positively associated with market size; Asia’s small and fragmented bond markets lack depth and liquidity because they fall well below the minimum scale needed to function efficiently.

Bond market standardization and harmonization through the ASEAN+3 Bond Market Forum can facilitate the integration of individual Asian bond markets to achieve the minimum efficient scale needed for market depth and liquidity.

So, are bonds the next big thing in financing Asia’s infrastructure needs? The short answer is, “not yet.”

Infrastructure bond market development lies at the confluence of two of the region’s most pressing strategic priorities: financing infrastructure and developing stable sources of long-term financing. As such, now is the right time for ASEAN+3 to press on with measures like CGIF to provide credit guarantees for infrastructure bonds, as well as other regional initiatives.

(Donghyun Park is Principal Economist, Economic Research and Regional Cooperation Department, Asian Development Bank)

08 Jan 2025 21 minute ago

08 Jan 2025 1 hours ago

08 Jan 2025 3 hours ago

08 Jan 2025 4 hours ago