18 Apr 2020 - {{hitsCtrl.values.hits}}

‘No data yet,’ he answered. ‘It is a capital mistake to theorise before you have all of the evidence. It biases the judgement.’

-Sherlock Holmes’ A Study in Scarlet

No data yet, apart from the distressing data on the escalating infections and deaths caused by the COVID-19 outbreak. The economic shock is yet to be seen.

No data yet, apart from the distressing data on the escalating infections and deaths caused by the COVID-19 outbreak. The economic shock is yet to be seen.

On March 16, 2020, China reported that in the two months of January and February alone there was a record 13.5 percent drop in the factory output. The World Bank, in a study released on March 30, 2020, projects the possibility of a massive increase in poverty levels in the East Asian and Pacific countries. The International Labour Organisation, in a study released on April 7, projects a massive increase in unemployment globally and calls for swift policy actions and open trade regimes.

Opinion pieces are abound that warn of dire outcomes in the absence of early policy interventions. Some even think that containing the pandemic quickly does not necessarily lead to a rapid

economic recovery.

The economic fallout of the COVID-19 outbreak at a global scale is likely to be unprecedented. We thought of engaging in such a global assessment to provide early projections of growth trajectories across countries that can shed some light on what to expect in the absence of policy interventions.

Brief methodology

For the analysis we use a large-scale econometric model that we constructed. It connects quarterly GDP growth of 60 economies (with one more representing the rest of the world) through 3660 bilateral export share series.

For the present analysis, we have to modify the model to account for the COVID-19 impact. The COVID-19 shock generates negative growth effects through disturbances to demand and supply channels.

On the one hand, increasing healthcare and other related fiscal expenditures is a boost to economic growth. On the other hand, many restrictions such as lockdown, curfew and travel restrictions imposed to contain the contagion entail both demand and supply disruptions at an international level.

At this stage, the required data to estimate the COVID-19-related parameters of the model are not yet available. We, therefore, adopt the framework of intervention analysis and calibrate these parameter values and combine them with the pre-crisis parameter values to run the full model. In the intervention framework, COVID-19 is represented by a binary dummy variable that can be set to one to generate long-run effects of the crisis.

We make brave assumptions to calibrate the parameter values. We first assume that the more the COVID-19 infections in a country, the severe the strain on the economy. Based on this, we use the proportion of COVID-19 infections in each country in the first quarter of 2020 (number of cases in a country divided by the total number of cases in the world) to represent the impact effect of COVID-19 on the

GDP growth.

For the second quarter of 2020, we assume an 80 percent reduction of the infections and for the third quarter, 99 percent reduction. These represent the lagged effect. Note that these are only parameter estimates; the full impact of the COVID-19 global shock is generated by running the full model interactively.

We generate a baseline growth scenario, where the direct impact of COVID-19 on each country is proportional to the infection proportion mentioned above. The baseline numbers can be multiplied by any desired number for each country to magnify the impact.

Although the magnitude of the fall in growth is important to assess the severity of the recession, at this stage, we draw more attention to the growth trajectory and duration of the downturn.

An important advantage of our model is that it can generate the direct growth effect of the COVID-19 shock on a country and the indirect growth effect that results through the international transmission of the recessionary impact.

Results

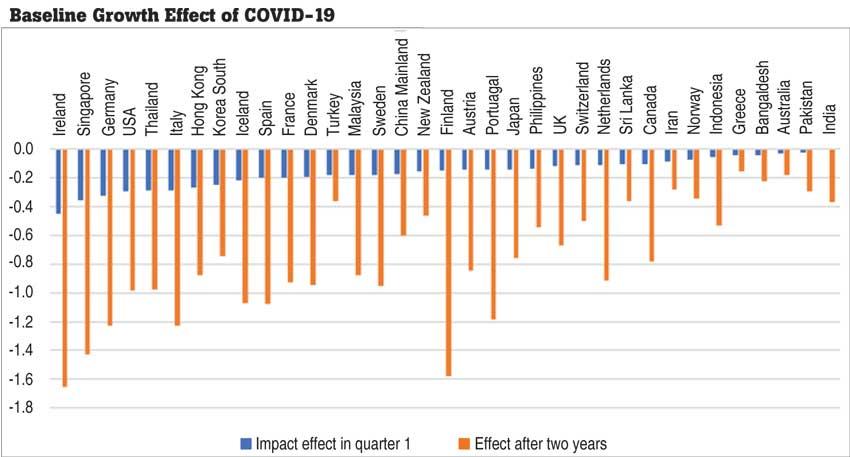

The chart shows by how much the GDP growth is going to drop over a two-year period for selected countries. The countries in the chart are ranked by the first quarter impact effect of COVID-19. It should be emphasised again that these numbers represent only a baseline case. Actual growth effect depends on the magnitude of demand and supply shocks each country is facing.

Overall, the exercise brings out the following general results.

First, although we assumed that the COVID-19 contagion withers away within three quarters, the economic contagion is going to continue in the absence of effective policy interventions. The baseline scenario projects mild recessionary conditions that may last two to four years in some countries. However, the duration depends on the severity of the downturn. The best hope is for a V shape recovery, if the COVID-19 contagion is contained as assumed and policy interventions for economic recovery work effectively.

Second, with the exception of few countries, 80 percent-99 percent of the drop in growth results from the international transmission effect (indirect effect), not from the direct impact of COVID-19. The countries that are less prone to international transmission of recessionary effects are Germany (75 percent), China (50 percent), Iran (39 percent) and the USA (26 percent).

Third, although the impact growth effect of COVOD-19 is very low for some countries like India, as time goes by, they also suffer as a result of disruptions to international transactions. The chart shows that the recessionary impact after two years changes the initial ranking pattern completely.

More specifically, highly open Singapore is more susceptible to the economic crisis caused by COVID-19 than Sri Lanka. However, during the past crises, Singapore rebounded very quickly because of effective and innovative policy interventions. Although Sri Lanka may be less affected relatively, Sri Lanka also needs innovative policy interventions to avoid a protracted downturn.

There is silver lining in the dark cloud. The global economic

downturn, instead of just a few countries suffering, generates the need for collective actions. When conditions improve with policy interventions, the international transmission mechanism renders faster recovery to all

the countries.

(Tilak Abeysinghe is Research Director of the Gamani Corea Foundation, Sri Lanka and was a Professor of Economics at the National University of Singapore. Shen Yifan is an Assistant Professor at the Institute of Politics and Economics, Nanjing Audit University, China)

25 Dec 2024 9 hours ago

25 Dec 2024 25 Dec 2024

25 Dec 2024 25 Dec 2024