04 May 2018 - {{hitsCtrl.values.hits}}

In 2015, 193 countries adopted the 17 Sustainable Development Goals (SDGs) as an overarching policy roadmap through 2030. These goals are predicated on the idea that for a sustainable future, economic growth must go hand-in-hand with social inclusion and protection of the environment.

In 2015, 193 countries adopted the 17 Sustainable Development Goals (SDGs) as an overarching policy roadmap through 2030. These goals are predicated on the idea that for a sustainable future, economic growth must go hand-in-hand with social inclusion and protection of the environment.

Our respective institutions, the United Nations Department of Economic and Social Affairs (UNDESA) and International Monetary Fund (IMF), fully support these goals. From the UN perspective, they represent a down payment on a more peaceful, prosperous and cooperative world, especially in increasingly perilous times. For the IMF, they help underpin economic stability and sustainable and inclusive economic growth.

In 2017, most types of development financing flows increased, helped by an upturn in the world economy, increased investment and supportive financial market conditions. Yet, less than three years after adoption, the implementation of the SDGs is running into a major hurdle—rising public debt in some developing countries. This is the sobering message of a new report on financing for development issued by the UN, in collaboration with the IMF and almost 60 other agencies.

Here’s the problem: as noted recently by IMF Deputy Managing Director Tao Zhang, 40 percent of low-income countries face high risk of debt distress or are unable to service their debt fully—this is up from 21 percent just five years ago. On top of this, several developing countries are also falling behind in terms of per capita income, induced by such factors as fragility and conflict—these include vulnerable countries like Haiti, D.R. Congo, and Chad.

Low tax revenue, weak international support

A key problem is that many of these countries are not able to raise enough public revenue. There are many reasons for this—narrow tax bases, continued over-reliance on extractive industries and weak tax administration. But tax evasion is also part of the problem. The low tax take in low income developing countries—where the median tax revenue is just 13.3 percent of gross domestic product—can be traced in part to informality and tax evasion.

In light of this, the first step of any reform strategy must surely be to raise more revenue at home. But in a world where business activity has become increasingly global, domestic efforts alone will not be enough. We will also need enhanced international collaboration on tax. It is encouraging that governments are developing new international standards on exchange of tax information—we need to make sure that developing countries also benefit from this.

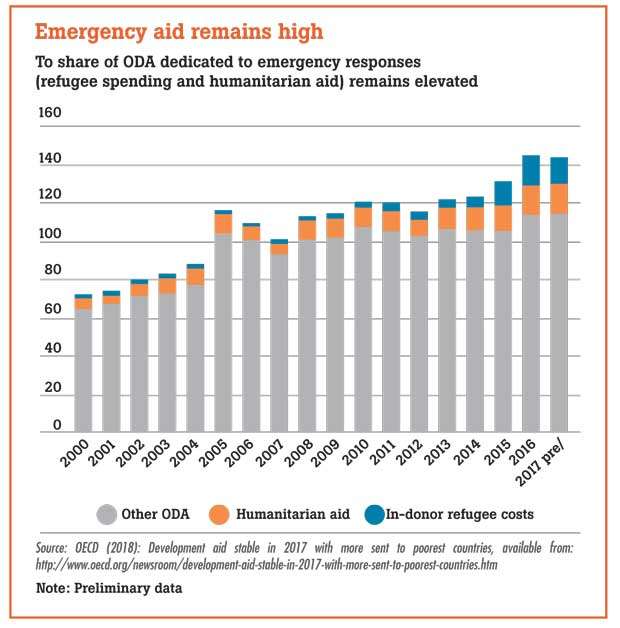

Official development assistance (ODA) also has a vital role to play. According to recently released data, ODA amounted to US $ 146.6 billion in 2017. But this amounts to less than half the internationally-agreed target of 0.7 percent of gross national income. And a growing share of ODA is being deployed for emergencies such as in-country refugee costs and humanitarian aid. While such aid is critical, it leaves less available for long-term public investments in sustainable development. ODA inflows toward the poorest and most vulnerable countries have stagnated and remain concentrated in a few of them. Donor countries need to step up their assistance in this area.

Private investment in support of SDGs

Given the large investment needs, attracting more private investment will be critical. But the least developed countries still struggle to do so at scale, particularly in sectors outside extractive industries. The report calls on developing countries to continue building competitive business environments, including by improving institutional and regulatory frameworks and developing project pipelines and investible projects—especially in infrastructure.

More recently, policymakers have also focused on sharing risks with private investors, through instruments such as guarantees and public-private partnerships. If done correctly, such blending activities can potentially unlock additional SDG investments. For now, they are mostly bypassing countries where the need is greatest. Only 7 percent of private finance so far mobilized was directed toward projects in the least developed countries.

There is also a risk that such activities will also add to debt burdens, including through contingent off-balance sheet liabilities. These risks need to be managed carefully.

Growing debt risks

The recent growth in debt is not all bad news, however. Greater access to international financial markets and lending by new creditors such as China, has unlocked the much-needed financing for infrastructure investments in recent years. And investment in productive capacity, if done right, can lead to higher income that offsets debt service. The report recommends that assessments of debt sustainability take this important channel into consideration.

But problems arise when debt is already high, when resources are not spent well (including in the presence of corruption and governance weaknesses) or when a country is hit by natural disasters or economic shocks such as sudden reversals of capital flows. Another issue is that the new wave of private credit often comes with higher interest rates and shorter maturities. And coordination among creditors has become harder, which creates problems when debt restructuring is needed.

When the risk of debt crisis is high, a quick response to lessen the immediate financial stress can make all the difference between rapid recovery and long-lasting harm. We need to think hard about innovative solutions here. For example, a greater use of state-contingent debt instruments—which reduce or delay a country’s debt obligations during crises—can provide some relief in some cases. By reducing default risks and risk premiums, they also expand available fiscal space

for investment.

Another interesting idea is debt-for-climate swaps—these entail concessional funders buying back outstanding debt, freeing up resources to fight climate change and helping regions hit hard by climate-related disasters.

Now is the time

The bottom line is that we only have 12 years left in which to implement the SDGs. The current upswing in the global economy opens up a vital window of opportunity but we must make sure that the financing agenda is not derailed by mounting public debt.

The UN and IMF are united in this common cause. This is demonstrated by our collaborative report, which puts forth recommendations on public finance and debt, private investments, trade and other critical priorities for SDG financing. Our institutions are committed to deepening our support for the SDGs, in the service of our member countries, to secure a more prosperous and peaceful world.

(Christopher Lane is Special Representative of the International Monetary Fund to the United Nations. Elliott Harris is United Nations Assistant Secretary-General for Economic Development and Chief Economist)

18 Nov 2024 1 hours ago

18 Nov 2024 1 hours ago

18 Nov 2024 2 hours ago

18 Nov 2024 6 hours ago

18 Nov 2024 7 hours ago