30 Apr 2021 - {{hitsCtrl.values.hits}}

Sri Lanka’s edible oil market has received considerable attention in recent weeks due to a series of events: the banning of palm oil importation in a bid to promote the coconut industry, detection of aflatoxins in imported coconut oil, importation of coconut kernel chips, issuing licence for palm oil imports and banning of oil palm cultivation.

Sri Lanka’s edible oil market has received considerable attention in recent weeks due to a series of events: the banning of palm oil importation in a bid to promote the coconut industry, detection of aflatoxins in imported coconut oil, importation of coconut kernel chips, issuing licence for palm oil imports and banning of oil palm cultivation.

The edible oil industry is important for Sri Lanka. Oils and fats are a major constituent of the typical Sri Lankan diet and a raw material in manufacturing, in particular the food manufacturing industry. According to the latest available data, there are around 5,057 establishments employing 332,828 workers in the formal food manufacturing sector, which generate an annual output of approximately Rs.1.4 billion. This article assesses the local edible oil market and its potential for import substitution.

Sri Lanka’s edible oil market

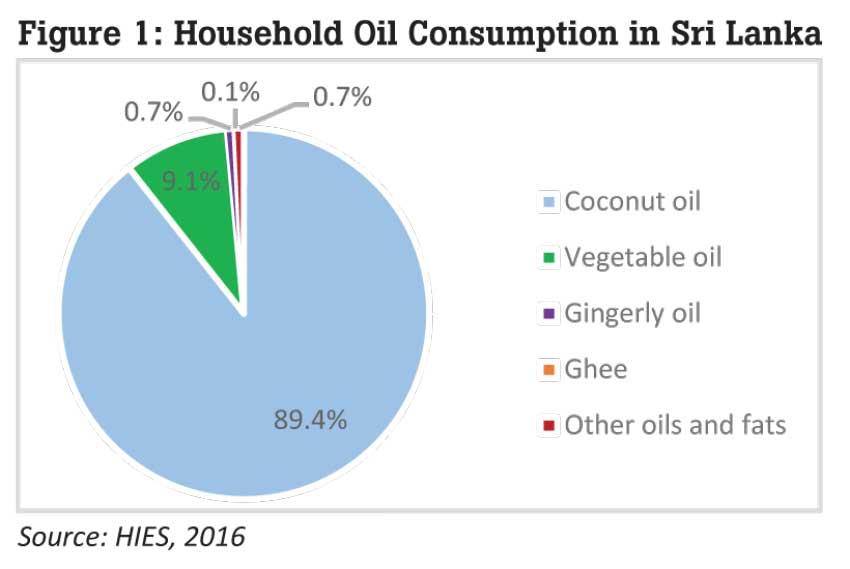

The demand for domestic edible oils comes from two segments: households and industries. Data from the 2016 Household Income and Expenditure Survey (HIES) of the Department of Census and Statistics (DCS) show that an average household consumes 1.6 litres of fats and oils per month and the annual consumer demand is around 96,249 MT, with coconut oil being the main source of edible oil (Figure 1). Industrial demand in 2020 can be approximated to 167,372 MT.

This demand for edible oils in the country is met by locally produced oils as well as imported oils. Coconut oil and palm oil are the local edible oil sources. In 2020, total edible oil production was 44,326 MT. Coconut oil production was 19,759 MT, which depends on annual coconut production. Crude palm oil and palm kernel oil production was 24,567, according to the Coconut Development Authority (CDA).

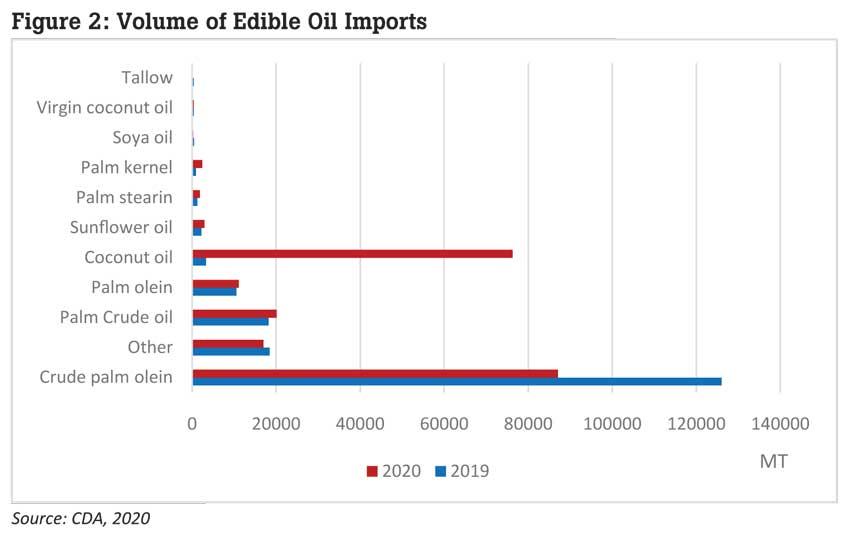

According to the CDA, the quantity of imported fats and oils in 2020 was 219,295 MT. A range of edible oils are imported to meet industrial demand and partially to meet household demand (Figure 2). The foreign exchange outflow in 2020 was Rs.37,378 million for edible oil imports.

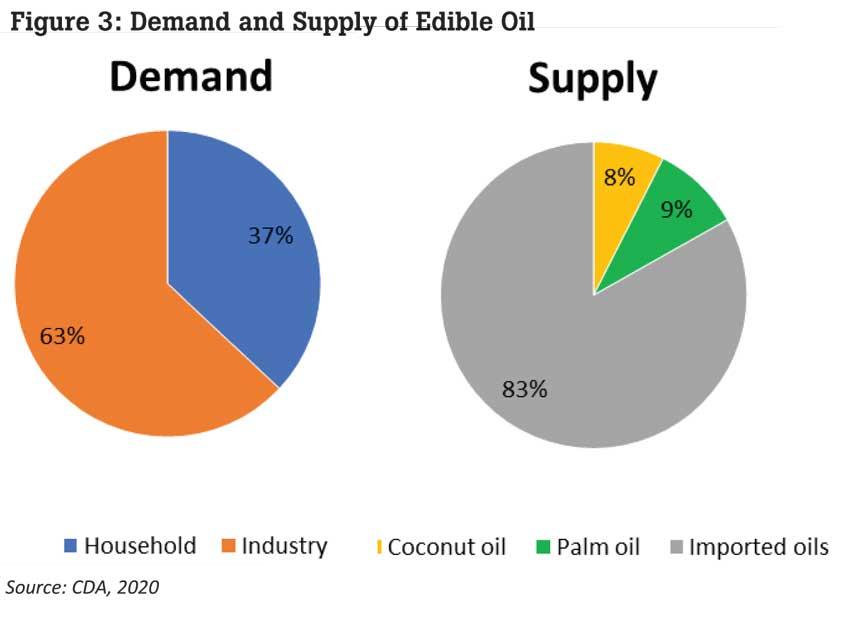

Total edible oil supply during 2020 was 263,621 MT, both from local production (44,326 MT) and imports (219,295). Around 83 percent of the requirement is met by imports and industrial demand is nearly two-thirds of the total demand (Figure 3).

The available data show that it is difficult to meet the edible oil demand from the local supply. The average coconut production during last five years was around 2,792 million nuts. Nearly 65-70 percent of the produce is consumed as fresh coconuts (1,800 million nuts). Processing industries utilise the remaining coconuts (around 1,000 million).

Around 108,108 MT of coconut oil can be produced from 1,000 million nuts at the expense of export industries, yet 155,513 MT of excess demand has to be met. Palm oil is cultivated in 12,000 ha, which is expected to produce nearly 48,000 MT. Together, coconut and palm oil can be expected to supply 156,108 MT of edible oil, which is still short of 107,513 MT of oil required to meet the consumer and industry demand.

Way forward

Given the current context, Sri Lanka cannot meet its edible oil demand as the coconut supply is not sufficient to meet the edible oil demand and expansion of production is difficult in the short term. Imported edible oils are an essential ingredient in food manufacturing, due to its unique properties and low cost. Therefore, facilitating importation is required to meet the local demand.

Sri Lanka spends around Rs.37 billion for edible oil imports and looking for alternatives is a sensible solution. Rice bran oil is a potential byproduct of paddy milling and it does not demand extra land for cultivation. Sri Lanka has to invest in utilising this potential resource. Measures to achieve optimum productivity from existing coconut lands are vital to reduce oil imports.

Investments have already been made in palm oil production. It is important to reinvestigate the concerns around palm oil cultivation. Oil palm being an exotic species, the impact on the local ecosystem is yet unknown with concerns of losing rubber lands, ground water depletion and effluent disposal. Palm oil is more efficient in oil production than coconut; one ha of oil palm produces nearly four MT of oil while coconut produces nearly one MT of oil. Limited availability of lands restricts further expansion of coconut lands. Therefore, a combination of coconut and oil palm can be considered to meet the demand for edible oil and the other products.

The coconut industry is directly influenced by edible oil importation. Imported edible oils are cheap, reduce the demand for local coconut oil and allow adulteration. However, the low cost is an advantage for manufacturing industries. Coconut being a multipurpose tree is incomparable to oil palm in food security and livelihoods terms. Promoting coconut export industries is economically attractive. Export income in 2020 from kernel products was Rs.63,293 million. Sri Lanka’s coconut products enjoy export demand and a competitive advantage due to its unique taste and colour. Thus, imported raw material is unlikely to be a substitute for export industries and the potential for earning foreign exchange would be low.

The present policy of permitting coconut oil imports under low tariff rates and kernel chips as a raw material to meet the household coconut oil demand while keeping the coconut oil millers in business can only be a short-term solution. Facilitating traditional millers to reach global virgin coconut oil (VCO) and lauric acid value chains will assure their competitiveness while rewarding the coconut growers with a reasonable price. Further, domestic coconut oil consumers may need to partially shift to substitute oils or imported coconut oil until coconut production is substantially increased. A comprehensive analysis to ascertain the cost benefits of using different types of edible oils for different purposes is a priority. Availability of these facts will help consumers make informed decisions, address misapprehensions and better ensure the well-being of all Sri Lankans.

(Erandathie Pathiraja is a Research Economist at the Institute of Policy Studies of Sri Lanka (IPS) with research interests in the analysis of industries and markets, competitiveness and SMEs. She holds a BSc in Agriculture from the University of Peradeniya, an MPhil in Agricultural Economics from the Postgraduate Institute of Agriculture and a PhD in Agricultural Economics from the University of Melbourne, Australia. She can be reached at [email protected])

23 Dec 2024 9 hours ago

23 Dec 2024 23 Dec 2024

23 Dec 2024 23 Dec 2024

23 Dec 2024 23 Dec 2024