22 Jan 2020 - {{hitsCtrl.values.hits}}

In the October World Economic Outlook, we described the global economy as in a synchronised slowdown, with escalating downside risks that could further derail growth. Since then, some risks have partially receded with the announcement of a US-China Phase I trade deal and lower likelihood of a no-deal Brexit. Monetary policy has continued to support growth and buoyant financial conditions. With these developments, there are now tentative signs that global growth may be stabilising, though at subdued levels.

In the October World Economic Outlook, we described the global economy as in a synchronised slowdown, with escalating downside risks that could further derail growth. Since then, some risks have partially receded with the announcement of a US-China Phase I trade deal and lower likelihood of a no-deal Brexit. Monetary policy has continued to support growth and buoyant financial conditions. With these developments, there are now tentative signs that global growth may be stabilising, though at subdued levels.

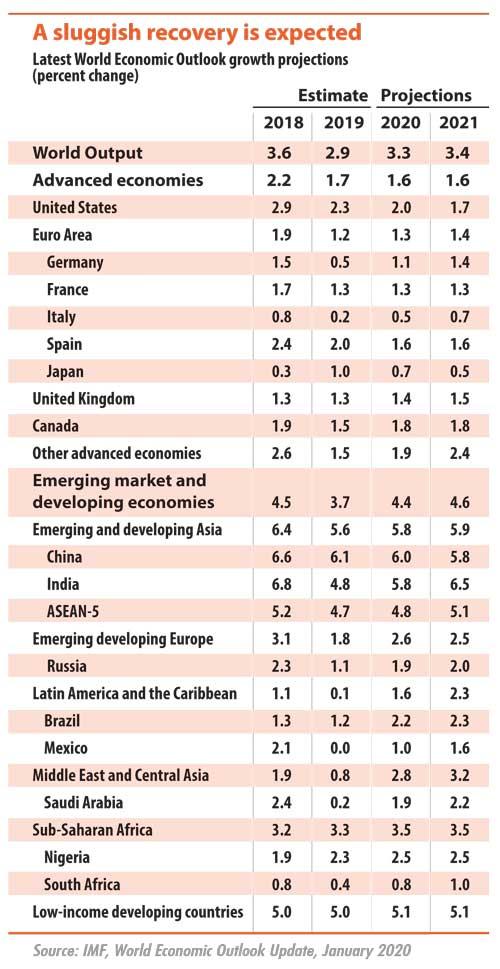

In this update to the World Economic Outlook, we project global growth to increase modestly from 2.9 percent in 2019 to 3.3 percent in 2020 and 3.4 percent in 2021. The slight downward revision of 0.1 percent for 2019 and 2020 and 0.2 percent for 2021, is owed largely to downward revisions for India. The projected recovery for global growth remains uncertain. It continues to rely on recoveries in stressed and underperforming emerging market economies, as growth in advanced economies stabilises at close to current levels.

There are preliminary signs that the decline in manufacturing and trade may be bottoming out. This is partly from an improvement in the auto sector as disruptions from new emission standards start to fade. A US-China Phase I deal, if durable, is expected to reduce the cumulative negative impact of trade tensions on global GDP by end-2020—from 0.8 percent to 0.5 percent.

The service sector remains in expansionary territory, with resilient consumer spending supported by sustained wage growth. The almost synchronised monetary easing across major economies has supported demand and contributed an estimated 0.5 percentage point to global growth in both 2019 and 2020.

In advanced economies, growth is projected to slow slightly from 1.7 percent in 2019 to 1.6 percent in 2020 and 2021. Export dependent economies like Germany should benefit from improvements in external demand, while US growth is forecast to slow as fiscal stimulus fades.

For emerging market and developing economies, we forecast a pickup in growth from 3.7 percent in 2019 to 4.4 percent in 2020 and 4.6 percent in 2021, a downward revision of 0.2 percent for all years. The biggest contributor to the revision is India, where growth slowed sharply owing to stress in the nonbank financial sector and weak rural income growth. China’s growth has been revised upward by 0.2 percent to 6 percent for 2020, reflecting the trade deal with the United States.

The pickup in global growth for 2020 remains highly uncertain as it relies on improved growth outcomes for stressed economies like Argentina, Iran and Turkey and for underperforming emerging and developing economies such as Brazil, India and Mexico.

Risks retreating but still prominent

Overall, the risks to the global economy remain on the downside, despite positive news on trade and diminishing concerns of a no-deal Brexit. New trade tensions could emerge between the United States and the European Union and US-China trade tensions could return. Such events alongside rising geopolitical risks and intensifying social unrest could reverse easy financing conditions, expose financial vulnerabilities, and severely disrupt growth.

Importantly, even if downside risks appear to be somewhat less salient than in 2019, policy space to respond to them is also more limited. It is therefore essential that policymakers do no harm and further reduce policy uncertainty, both domestic and international. This will help to revive investment, which remains weak.

Policy priorities

Monetary policy should remain accommodative where inflation is still muted. With interest rates expected to stay low for long, macroprudential tools should be proactively used to prevent the build-up of financial risks.

Given historically low interest rates alongside weak productivity growth, countries with fiscal space should invest in human capital and climate-friendly infrastructure to raise potential output. Economies with unsustainable debt levels will need to consolidate, including through effective revenue mobilisation. To ensure a timely fiscal response if growth were to slow sharply, countries should prepare contingent measures in advance and enhance automatic stabilisers. A coordinated fiscal response may be needed to improve the effectiveness of individual measures. Across all economies, a key imperative is to undertake structural reforms, enhance inclusiveness and ensure that safety nets protect the vulnerable.

Countries need to cooperate on multiple fronts to lift growth and spread prosperity. They need to reverse protectionist trade barriers and resolve the impasse over the World Trade Organisation’s appellate court. They must adopt strategies to limit the rise in global temperatures and the severe consequences of weather-related natural disasters.

A new international taxation regime is needed to adapt to the growing digital economy and to curtail tax avoidance and evasion, while ensuring that all countries receive their fair share

of tax revenues.

To conclude, while there are signs of stabilisation, the global outlook remains sluggish and there are no clear signs of a turning point. There is simply no room for complacency and the world needs stronger multilateral cooperation and national-level policies to support a sustained recovery that benefits all.

(Gita Gopinath is Economic Counsellor and Director of the Research Department at the International Monetary Fund)

26 Dec 2024 18 minute ago

26 Dec 2024 24 minute ago

26 Dec 2024 1 hours ago

26 Dec 2024 1 hours ago

26 Dec 2024 4 hours ago