09 Jan 2013 - {{hitsCtrl.values.hits}}

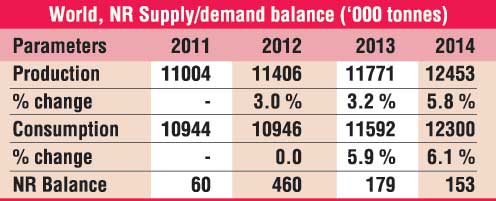

.jpg) The latest report of the International Rubber Study Group ( IRSG ) says that the world total rubber consumption contracted in the in the 3rd quarter of 2012, decreasing to 25.7 million tonnes on a moving annual total (MAT) basis in September 2012, from 25.9 million tonnes on a MAT basis in June 2012.

The latest report of the International Rubber Study Group ( IRSG ) says that the world total rubber consumption contracted in the in the 3rd quarter of 2012, decreasing to 25.7 million tonnes on a moving annual total (MAT) basis in September 2012, from 25.9 million tonnes on a MAT basis in June 2012..jpg)

26 Nov 2024 9 minute ago

26 Nov 2024 43 minute ago

26 Nov 2024 1 hours ago

26 Nov 2024 1 hours ago

26 Nov 2024 2 hours ago