Investing in real estate has been the traditional method of securing future financial stability by increasing one’s net worth. With the advent of share trading, investments in property have been in direct competition to attract investment rupees.

Bricks and mortar or shares was the toss up considered by many investors as they pondered the risks and benefits of each. For many though, investing in real estate, particularly commercial real estate, is financially out of scope.

But what if you could pool your resources with other investors and invest in large-scale commercial real estate as a group? Real estate investment trusts, commonly known as REITs, (pronounced like ‘treats’) allows you to do just that. They offer the benefits of real estate ownership without the headaches or expense of being a landlord.

The Securities and Exchange Commission (SEC) together with the Colombo Stock Exchange (CSE) is currently discussing the formation and structures of REITs as a new product with several market participants who have shown an interest in launching such an investment vehicle in the context of Sri Lanka’s property environment.

Types of REITs

REITs are corporations/trusts that own and manage a portfolio of real estate-based assets. Typically there are two main types of REITs - Equity REITs (own and operate income-producing real estate) and Mortgage REITs (lends money directly to real estate owners and their operators or indirectly through acquisition of loans or mortgage-backed securities). REITs that engage in both of these product features are commonly known as Hybrid REITs.

Investments in REITs are generally designed to create the important advantages of ‘liquidity’ and ‘diversity’. Unlike actual real estate property, these shares can be quickly and easily sold. And because you’re investing in a portfolio of properties rather than a single building, risk elements are mitigated.

Property types such as office spaces, shopping malls, apartments, warehouses, healthcare complexes, theatres and even mixed commercial spaces are eligible to makeup the core asset base of a REIT.

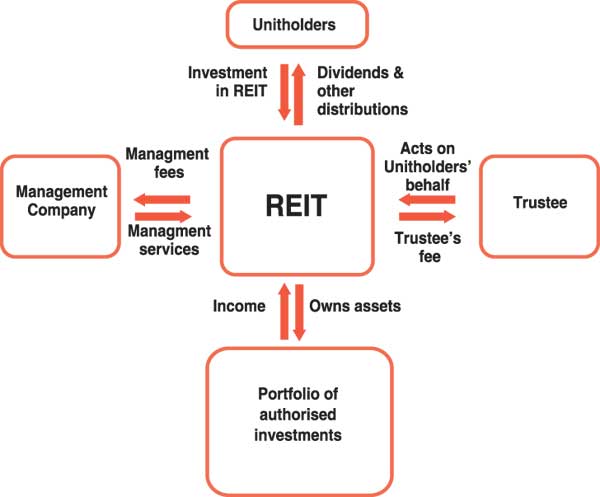

A simplified example of an Equity REIT generally consists of four key components.

1.A company/trustee that owns and operates income-producing real estate:

The trustee acts on behalf of the unit holders and in return takes a trustee fee.

2.An authorized portfolio of core investments/assets that are made available to be parcelled into the REIT offering:

These assets generate the all-important income stream from which investors are able to derive their returns.

3.A property management company to provide management services required by the portfolio of properties.

Receives a management fee in return.

4.Lastly, but most importantly – the unit holders.

3A pool of investors (minimum numbers determined to ascertain eligibility of a REIT) who invest in a REIT product and receive dividends and other distributions.

An illustration of the above is as follows:

Benefits offered

REITs came about in 1960, when the US Congress decided that smaller investors should also be able to invest in large-scale, income-producing real estate. It determined that the best way to do this was to follow the model of investing in other industries -- the purchase of ‘equity’.

The engagement of the SEC and CSE with proponents of this investment vehicle contends with the legal framework for operation and issues such as a proposed lobby to avoid double taxation at the corporate and individual level. In countries such as the US, Australia, Singapore and Malaysia taxes on the core asset of a REIT product is passed onto the individual investor.

As there is an increased demand for commercial office space in Sri Lanka, which is largely driven by the banking, IT and tourism sectors, astute product suppliers have realized the opportunity to extend the benefits of real estate to investors who would otherwise not have the capacity to have property on their investment portfolios.

REITs offer several other benefits over actually owning properties.

They are highly liquid. In other words, while it’s difficult and time-consuming to buy, rent and sell houses on your own, this isn’t the case with REITs, which can be bought and sold as easily as stocks.

REITs enable you to own a share in non-residential properties as well, such as hotels, malls and other commercial or industrial properties.

Lastly, the minimum investment with a REIT is comparatively lower and investors can start small and increase their exposure over time by gauging the performance of the product invested into.

In most cases these types of investment vehicles have delivered higher yields than benchmark investments in most global investment platforms. In the US for example, REIT products during a 20-year span from 1990 to 2010 consistently outperformed 10-year Treasury bonds.

Risks involved

As is the case with any investment a REIT too has inherent risks that an investor should be aware of. A drop in the price or valuations of a property will have an adverse effect on the price of the units of a REIT whilst low occupancy in the core assets will affect the distributed income stream. Other potential risks to be considered are insufficient diversification, tenancy durations and the quality of tenants.

The SEC hopes to pique the interest of many target stakeholders to enter the capital market through the introduction of a REIT product.

Institutional investors

Property companies that own income generating properties

Banks that have exposure to property

Portfolio and asset management companies

Property developers

Foreign investors

Regulatory framework

Currently there is robust engagement around the introduction of these products including the regulatory framework necessary to protect potential investors. A study of the initial entry and performance of these products in similar markets is also being carried out by the SEC with learning outcomes expected to assist the formation of relevant governing rules in context of the Sri Lankan markets.

The SEC expects to coordinate a consultative process with other key organisations and regulatory bodies to formalize such key requirements as accounting standards, taxation rules, defined responsibilities of key stakeholders, dividend policies, valuations, reporting processes and the rights of investors of these products.

.jpg)