The international management consultancy MTI recently concluded its 4th CEO Business Outlook Survey, with the results officially revealed by MTI International CEO Hilmy Cader, at CIMA Corporate Partners Launch 2015.

Augmented by MTI Consulting’s thought leadership initiatives and key learnings derived from its consulting experience over the years, the survey analysed and assessed the perceptions of over 150 Sri Lankan chief executives with regard to the past success and expected future success of their companies, their predictions regarding the state of the local and global economy in 2015 and the challenges their business as well as the Sri Lankan economy are likely to face.

The results of this survey will enable companies to streamline their strategizing for 2015 and aid them in their key decisionmaking process - with regard to adding mass or trimming down, expanding or tightening, competitively attacking or defending and progressing on a rampage or taking cover.

.jpg)

Significant improvements or lower expectations?

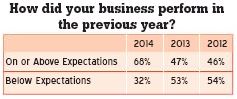

Approximately 68 percent of surveyed CEOs stated that their business performed on or above expectations for 2014, while 32 percent stated that performance was below expectations. This is in sharp contrast to the results of the previous year where only 47 percent of the CEOs saw performance meet or exceed their expectations while the remainder failed to meet their expected targets.

This poses an important question – has there been a significant improvement in business performance over the last financial year or did CEOs simply lower their expectations at the beginning of the year to be able to meet their sub-standard targets at the end?

Through a quick analysis of the September quarterly reports for the S&P20 and a sample of small to mid-cap (S&M) firms – 90 percent of the S&P20 have enjoyed a year-on-year (YoY) growth in net earnings while only 40 percent of S&M firms have experienced a YoY dip in net earnings. This does therefore provide some evidence of an improvement in business performance for 2014.

There are, however, a few concerns that must be addressed. Firstly, the business environment has been subject to slow credit growth in 2014. Borrowing at especially the small and medium enterprise (SME) level has reduced significantly in spite of the reduction in interest rates and attractive campaigns run by banks.

Secondly, despite banks promoting credit, the non-performing accommodation ratios have i ncreased. Thirdly, t he bottom of pyramid is a blue ocean in terms of livelihood products (especially credit products). There has been insufficient focus on this socioeconomic segment which may sharply shift in the future as the current government places a lot more emphasis on improving their lives.These are a few concerns that need to be kept in mind as we progress through 2015, regardless of the optimism vehemently displayed in the media.

Global economy will slip further

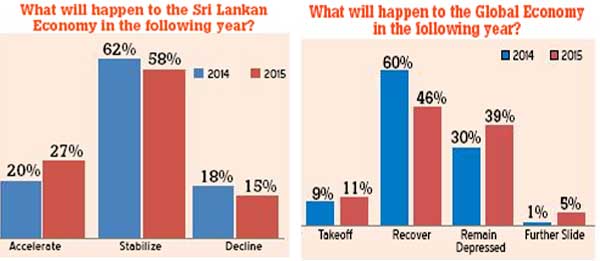

The opinion of Sri Lankan CEOs is that the global economy will slip further in 2015. As opposed to the results from 2014, a lesser proportion of CEOs (46 percent compared to 60 percent previously) expect a global recovery and a greater percentage expects a depression to continue (39 percent compared to 30 percent previously) or further worsen (5 percent compared to 1 percent previously). There has been an insignificant rise in the amount of CEOs expecting the economy to take-off in the current year (11 percent compared to 9 percent previously).

On the other hand, the World Bank and the International Monetary Fund (IMF) both predict that the world’s economy will enjoy a greater growth rate than 2014 – 3.0 percent and 3.5 percent, respectively – albeit only a respective 0.4 and 0.2 percentage points increment from the previous year.

However, as per the IMF, much of this global growth is to emanate from advanced economies that are estimated to grow at 2.4 percent in the current year – mainly on the back of a strengthening US economy - as opposed to their growth rate of 1.8 percent in the previous year. Developing and emerging economies, however, are estimated to grow at 4.3 percent in the current year, down from 4.4 percent in the previous year, mainly due to declining Chinese growth and lessening exports to the Eurozone.

Sri Lankan economy will marginally improve

A combined 85 percent of surveyed CEOs expect the Sri Lankan economy to either stabilize or accelerate while only 15 percent expect the economy to decline. Along the same lines, there has been a marginal reduction in CEOs expecting the economy to stabilize (58 percent compared to 62 percent previously) or decline (15 percent compared to 18 percent previously) and a noticeable increase in CEOs expecting the economy to accelerate in 2015 (27 percent compared to 20 percent previously).

This is once again surprising as the performance of the Sri Lankan economy depends greatly on domestic consumption and exports to the European Union (EU), of which the former is subject to the effects of slow credit growth while the latter is currently plagued by low flation and declining consumer spending. Clearly, CEOs expect vast improvements in these key areas in 2015.

Subdued expectations for 2015

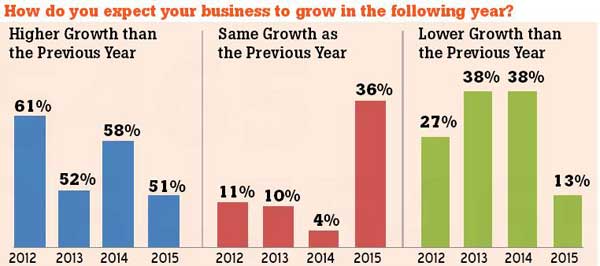

The pre-election business expectations for 2015 are quite subdued. There has been an extremely sharp increase in CEOs expecting the same growth as in the previous year for 2015 – that is 36 percent compared to the 8 percent average for the previous three years. Similarly, CEOs expecting lower growth than the previous year have dropped sharply from 38 percent in 2014 to only 13 percent in 2015. Those CEOs expecting higher growth than the previous year have remained volatile in number - with 51 percent saying so, almost similar to the amount in 2013, but a slight drop from 58 percent in 2014.

Overwhelmingly governance and political influence

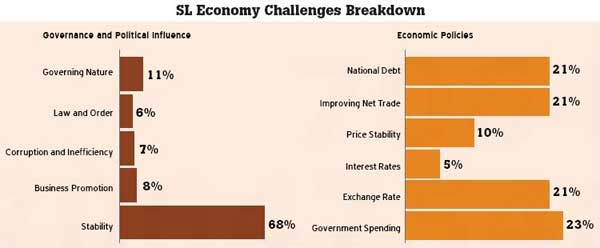

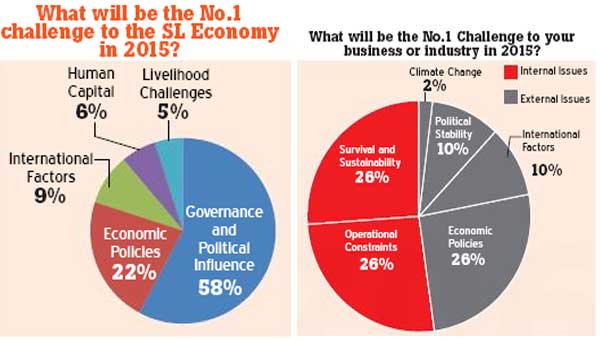

An outstanding 58 percent of CEOs believe that the primary challenge to the Sri Lankan economy is governance and political i nfluence, t hen followed by economic policies (which does share some similarities with the former) and a minor focus on i nternational factors, human capital and livelihood challenges in that order.

A closer look at governance and political influence unveiled a plethora of related sub-factors. While a primary problem was the stability of system, there were also several responses with regard to law and order, the nature of governance or in other words the transparency and consistency of their policies, corruption and inefficiency and the lack of development in certain sectors and industries and general business promotion.

Similarly, economic policies too were categorized into six sub-factors of which controversial government spending held the highest relative proportion, closely followed by national debt, improving net trade and exchange rates. There was less of a focus, however, on price stability and interest rates.

This raises the question – is the private sector sufficiently lobbying for the fundamental reforms needed for the prolonged success of the economy?

“The problem is out there, not with us!”

A significant number of CEOs (48 percent) believe that the primary challenge to their business is external and hence uncontrollable. These external factors are made up of economic policies, political stability, international factors and climate change. Do these external factors actually have an overbearing influence or are a significant proportion of respondents simply looking for the easy way out and blaming the government, its policies and the global economy for their shortcomings?

The majority of CEOs (52 percent) however, do believe that the primary challenge to their business in 2015 is internal. These internal factors are made up of operational constraints and survival and sustainability. Although it may be argued that the latter has external elements, it is the opinion of the author that a business’ survival in a competitive environment (and going concern) is majorly dictated by their competitive advantage and their product/service differentiation. As these in turn are influenced by a business’ flexibility and willingness to adapt to a dynamic environment – they are mainly internal issues. Of the operational constraints, the inability to identify and employ adequate human resources was the most widely cited reason, which poses the question – does Sri Lanka have a human capital problem and is it suffering the consequences of increasing brain drain? Rising costs, issues with handling and obtaining credit and corporate debt and corporate governance were also cited challenges.

The majority of CEOs (52 percent) however, do believe that the primary challenge to their business in 2015 is internal. These internal factors are made up of operational constraints and survival and sustainability. Although it may be argued that the latter has external elements, it is the opinion of the author that a business’ survival in a competitive environment (and going concern) is majorly dictated by their competitive advantage and their product/service differentiation. As these in turn are influenced by a business’ flexibility and willingness to adapt to a dynamic environment – they are mainly internal issues. Of the operational constraints, the inability to identify and employ adequate human resources was the most widely cited reason, which poses the question – does Sri Lanka have a human capital problem and is it suffering the consequences of increasing brain drain? Rising costs, issues with handling and obtaining credit and corporate debt and corporate governance were also cited challenges.

Global growth or more precisely the lack of it was seen as the most common international factor challenging the success of Sri Lankan businesses in 2015. Oil prices, which have been plummeting over the past few months, were the least common international challenge, while disruptive trends (for example, the ever changing supply chain) and currency volatility (excluding the SLR) fell in between.

Way forward for Sri Lankan businesses

There is no doubt that 2015 will require Sri Lankan companies to consider re-strategizing.The next few years will see fairly stable presidential policies but companies need to expect highly dynamic parliamentary politics. As we don’t know how this will turn out, it is important to possess or gain the ability to handle uncertainty amidst some certainty.

The current regime’s policies seem to place great focus on serving the basic needs of the people and catering to the bottom of the pyramid. Industries such as agriculture and food, healthcare, public transportation (not necessarily highways), affordable housing, micro-finance and other industries that employ semi-skilled labour (outside of the Western Province) are clearly set to be the promising growth zones in the future.

Another factor we need to keep in mind is the Sri Lankan rupee. Do we continue to pay the cost of holding it at its current value or do we let it float and experience the consequences? Though exporters may be satisfied at the moment, we’ll certainly have to pay at some point for the increasing cost of holding it now.

The energy bill for countries such as Sri Lanka will be significantly lower in 2015. Whether the entire saving will be passed on to the consumer is another question. However, despite the reduction in the energy bill, in the Sri Lankan context, the cost of ‘energizing’the refinery and the distribution could still be very inefficient.

Therefore, what benefits we gain from the reduction in oil prices may be lost during the refining and distribution process. Exports are to become extremely crucial as there will be less inflow in terms of infrastructure-based funding. Though there may be significant pressure to improve exports, this cannot be done efficiently during a 100-day plan. Fundamental policy changes are required in order to identify Sri Lanka’s competitive advantages. Perhaps the government will provide short-term incentives in order to drive exports further. Finally, those businesses which have become ‘addicted’ to ‘political sweeteners’ will have to re-think and re-skill themselves as without these ‘political sweeteners’ survival will become their primary challenge.

Hopefully, however, the system will not be reconfigured to how it once was and this may be the opportunity to drive Sri Lankan companies to survive on their own strength and skill in a level playing field and thereby not rely on political clutches to take their business forward. CEO Business Outlook Survey 2015 was carried out by MTI Consulting in association with the Chartered Institute of ManagementAccountants and enabled by Sarva Integrated, Daily Mirror, Daily FT and the SundayTimes.