25 Nov 2014 - {{hitsCtrl.values.hits}}

Natural gas is creating a new reality for economies around the world.Three major developments of the past few years have thrust natural gas into the spotlight: the shale gas revolution in the United States, the reduction in nuclear power supply following the Fukushima disaster in Japan, and geopolitical tensions between Russia and Ukraine.

WHAT’S COOKING?

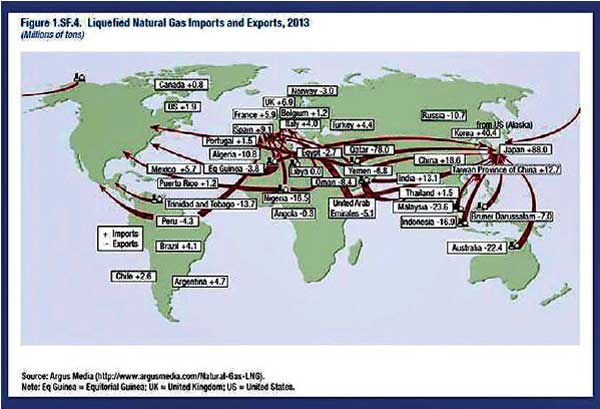

Over the last decade, the discovery of massive quantities of unconventional gas resources around the world has transformed global energy markets, and reshaped the geography of global energy trade (see map). Consumption of natural gas now accounts for nearly 25 percent of global primary energy consumption. Meanwhile, the share of oil has declined from 50 percent in 1970 to about 30 percent today.

Natural gas, however, is different from other energy sources. Being lighter than air, it is a commodity that doesn’t travel very easily and is expensive to transport. Hence, natural gas markets tend to be regional, and much less integrated than oil markets. Shipping or transporting natural gas requires either costly pipeline networks or liquefaction infrastructure and equipment, including dedicated vessels, and then re-gasification at the destination. The limited global integration of gas markets has resulted in substantial price differences across regions in recent years due to the U.S. shale gas boom and the Fukushima disaster, in spite of increasing liquefied natural gas trade.

U.S. SHALE GAS REVOLUTION

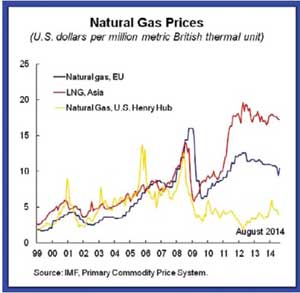

With advances in shale rock drilling, a sharp surge in U.S. gas production has made the country the world’s largest natural gas producer, and soon expected  to become a net exporter of natural gas. The shale gas boom has also had a significant impact on the patterns of global energy trade: U.S. fossil fuel imports decreased to $225 billion in 2013 from $412 billion in 2008.Surging supply has also steeply driven down natural gas prices in the United States by about 70 percent in recent years, introducing substantial price differences across other regions (see chart). For instance, U.S. gas sells for $4 per million British thermal units, compared with $10 in Europe and close to $17 in Asia.The U.S. advantage i n natural gas has also led t o an i ncrease i n U.S. competitiveness in non-energy products, in turn affecting its competitors.The share of energy-intensive manufacturing exports in t otal U.S. manufacturing exports has been rising steadily, whereas the share of non-energy intensive exports has been declining.Estimates show that cheaper natural gas in t he United States has helped lift manufacturing exports by about 6 percent since the start of the shale gas boom. Further evidence suggests that the channels through which cheaper domestic natural gas prices in the United States might have an impact on manufacturing exports are operating both at the intensive (expansion by existing firms) and extensive (new firm entry) margins.

to become a net exporter of natural gas. The shale gas boom has also had a significant impact on the patterns of global energy trade: U.S. fossil fuel imports decreased to $225 billion in 2013 from $412 billion in 2008.Surging supply has also steeply driven down natural gas prices in the United States by about 70 percent in recent years, introducing substantial price differences across other regions (see chart). For instance, U.S. gas sells for $4 per million British thermal units, compared with $10 in Europe and close to $17 in Asia.The U.S. advantage i n natural gas has also led t o an i ncrease i n U.S. competitiveness in non-energy products, in turn affecting its competitors.The share of energy-intensive manufacturing exports in t otal U.S. manufacturing exports has been rising steadily, whereas the share of non-energy intensive exports has been declining.Estimates show that cheaper natural gas in t he United States has helped lift manufacturing exports by about 6 percent since the start of the shale gas boom. Further evidence suggests that the channels through which cheaper domestic natural gas prices in the United States might have an impact on manufacturing exports are operating both at the intensive (expansion by existing firms) and extensive (new firm entry) margins.

As more countries exploit new sources of natural gas, not only is the geography of trade in energy products likely to continue to change, but the geography of manufacturing exports is likely to change as well.While energy users in the United States have been the main beneficiaries of the energy price declines, the shale revolution has helped to stabilize international energy prices including by freeing global energy supply for European and Asian markets, offsetting some of the shortages due to geopolitical disruptions.

THE FUKUSHIMA DISASTER AND AFTER MATH

The Fukushima Daiichi nuclear disaster in March 2011 highlighted the environmental liabilities associated with nuclear power generation, and induced a sharp increase in the use of natural gas.Before the disaster, about one-quarter of Japan’s energy was generated by means of nuclear reactors. Following the disaster, the Japanese government decided to halt production at all nuclear power plants in the country. To compensate for the resulting loss in electricity generation, Japanese electric power companies increased their use of fossil-fuel power stations and appended natural gas turbines to existing plants.

As a result, Japan’s liquefied natural gas imports have increased dramatically— by about 40 percent—since the disaster, making Japan the world’s largest importer of liquefied natural gas. The sharp increase in natural gas demand has led to higher prices in Asia—and Japan in particular— double that in Europe and four times higher than in United States.

GEOPOLITICAL TENSIONS

The ongoing crisis in Ukraine has highlighted European energy markets’ dependence on natural gas. Ukraine and countries in southeast Europe appear particularly vulnerable to potential disruptions of Russian gas supply.Should the gas cutoffs persist and be extended to other countries, the greatest impact will be on Ukraine and countries in southeast Europe that receive Russian gas transiting through Ukraine. Other countries, however, will be affected through rising spot prices, which may spread from natural gas to other fuels.

FUEL FOR THOUGHT

Overall, the pattern of global trade in liquefied natural gas, and energy more generally, is expected to evolve further. If the United States gradually becomes a net exporter of liquefied natural gas, we expect domestic natural gas prices to rise but still remain markedly lower than that in Europe and Asia, given liquefaction costs.

Natural gas is the cleanest source of energy among other fossil fuels (petroleum products and coal) and does not suffer from the other liabilities potentially associated with nuclear power generation. The abundance of natural gas could thus provide a “bridge” between where we are now in terms of the global energy mix and a hopeful future that would chiefly involve renewable energy sources.

While markets forces shape the energy mix, energy policy has a role to play, including for coal and renewable, in turn impacting global trade in energy. Here, Europe and Japan are at a crossroads, facing a difficult balance between environmental concerns, economic efficiency goals and energy security. Getting that balance right should figure prominently on policy makers’ agendas.

(Rabah Arezki heads the commodities team in the IMF’s Research Department. Rabah has written on commodities, international macroeconomics, and development economics. He has led and participated in various IMF missions in Africa, the Middle East and Central Asia)

25 Nov 2024 19 minute ago

25 Nov 2024 31 minute ago

25 Nov 2024 33 minute ago

25 Nov 2024 34 minute ago

25 Nov 2024 42 minute ago