13 Aug 2013 - {{hitsCtrl.values.hits}}

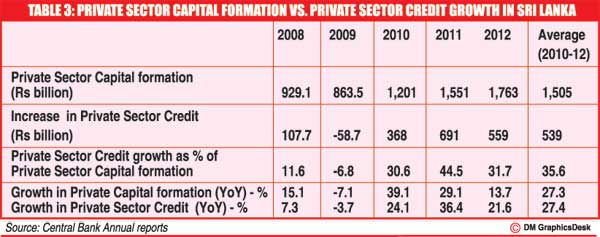

.jpg) Sri Lankan enterprises – especially SMEs use a comparatively high level of bank borrowings to fund investments. This is partly due to low level of domestic savings and inefficiency in the capital market.

Sri Lankan enterprises – especially SMEs use a comparatively high level of bank borrowings to fund investments. This is partly due to low level of domestic savings and inefficiency in the capital market.

.jpg)

.jpg)

26 Nov 2024 8 minute ago

26 Nov 2024 58 minute ago

26 Nov 2024 2 hours ago

26 Nov 2024 2 hours ago

26 Nov 2024 2 hours ago