08 Jun 2021 - {{hitsCtrl.values.hits}}

Protest held by Free Women with the slogan ‘Can’t pay - Won’t Pay’ to assist women gripped by the micro finance crisis

Protest held by Free Women with the slogan ‘Can’t pay - Won’t Pay’ to assist women gripped by the micro finance crisis

A milkman positioned ahead of us, ringing the bell on his bicycle every now and then, while on his routine delivery round. The golden rays of the morning sun have exposed enigmatic rock forms dominating the backdrop of the iconic Parakrama Samudra. We were in Polonnaruwa, the land of an ancient kingdom praised for its vast irrigation network and engineering marvels. But centuries later, this once flourishing kingdom is now a poverty-stricken district as many people are unable to make ends meet with mounting economic hardships and health conditions such as kidney failure. Therefore while men continue with farming, coolie work and brick making, women have opted to obtain loans from (mostly unregulated) micro finance companies. However, it was too late when they realised that it was a life-threatening trap. People in many areas from Maha Rathmale to Rotawewa, Hingurakgoda, Hen Yaya, Lankapura, Elahera, Debarella, Aralaganwila, Bakamuna and Welikanda have largely been affected by this crisis.

A milkman positioned ahead of us, ringing the bell on his bicycle every now and then, while on his routine delivery round. The golden rays of the morning sun have exposed enigmatic rock forms dominating the backdrop of the iconic Parakrama Samudra. We were in Polonnaruwa, the land of an ancient kingdom praised for its vast irrigation network and engineering marvels. But centuries later, this once flourishing kingdom is now a poverty-stricken district as many people are unable to make ends meet with mounting economic hardships and health conditions such as kidney failure. Therefore while men continue with farming, coolie work and brick making, women have opted to obtain loans from (mostly unregulated) micro finance companies. However, it was too late when they realised that it was a life-threatening trap. People in many areas from Maha Rathmale to Rotawewa, Hingurakgoda, Hen Yaya, Lankapura, Elahera, Debarella, Aralaganwila, Bakamuna and Welikanda have largely been affected by this crisis.

In this backdrop, the Daily Mirror met with a few micro finance beneficiaries in Maha Rathmale and Welikanda who shared their experiences with us.

Polonnaruwa plagued by a crisis

While around 2.8 million families across the island have been affected by this crisis, some 1,02,000 women in Polonnaruwa alone have been victimised. According to unofficial statistics, around 200 women have already taken their lives. Subsequently a 55-day satyagraha campaign was held in Hingurakgoda to voice out injustices faced by women when obtaining micro finance loans. Another campaign was launched by Free Women, a leftist women’s movement struggling for women’s freedom to obtain 10,000 signatures and the campaign was conducted in Kalutara, Puttalam, Polonnaruwa, Trincomalee, Badulla, Ampara and Moneragala districts.

While around 2.8 million families across the island have been affected by this crisis, some 1,02,000 women in Polonnaruwa alone have been victimised. According to unofficial statistics, around 200 women have already taken their lives. Subsequently a 55-day satyagraha campaign was held in Hingurakgoda to voice out injustices faced by women when obtaining micro finance loans. Another campaign was launched by Free Women, a leftist women’s movement struggling for women’s freedom to obtain 10,000 signatures and the campaign was conducted in Kalutara, Puttalam, Polonnaruwa, Trincomalee, Badulla, Ampara and Moneragala districts.

One of their main complaints is that during the election period contestants from both parties promised that they would exempt people from their micro finance debts. This was mainly for people who have obtained less than Rs. 100,000. Although it was just another promise, it was a ray of hope for people who were burdened by the issue. As a result people decided to stop paying off their debts and voted for these contestants placing their trust on mere promises. But to their dismay, by then the matter has blown out of proportion.

During the period they didn’t pay, more interests have accumulated to their installments. Therefore a Rs. 5000 installment has become Rs. 35,000 with the accumulated interest. People therefore had to pay bulk amounts to clear off their interests. Even though most people have settled the initial loan they have obtained, they are continuing to settle their interests. To date, most micro finance companies haven’t been clear about how they calculate their interests except the fact that interests could be anywhere between 40-220%. One of the justifications is that micro finance companies need money to operate given that they are located in remote areas and employ a larger staff. Following these revelations the Central Bank introduced an interest cap of 35% in 2018.

The other issue is that of collateral. In the case of government workers they could produce their pay cheques as collateral, but this is not the case when it comes to self-employed people. Most women don’t have assets and there is no formal collateral in this process. Usually groups of women are responsible for each other’s loans. In worst case scenarios women will keep a television set owned by the father or an asset owned by the husband as collateral.

Some debt-collectors have allegedly resorted to unethical practices in order to obtain debts. Most women go through harassment. Some dealers have allegedly gone to the extent of requesting for sexual bribes with promises to relieve women from their debt burden. The Daily Mirror came to know of instances where women and children go into hiding the moment they spot a dealer coming to their doorstep and pretend they are not at home until he leaves. As a result there are mounting number of family disputes and cases of domestic violence in the area. Even though their spouses agree to the idea of obtaining micro finance loans, they leave it to the women to settle payments as well. With no support from spouses and with mounting social pressure, women find it a challenge to carry the burden and opt to take their lives.

Some debt-collectors have allegedly resorted to unethical practices in order to obtain debts. Most women go through harassment. Some dealers have allegedly gone to the extent of requesting for sexual bribes with promises to relieve women from their debt burden. The Daily Mirror came to know of instances where women and children go into hiding the moment they spot a dealer coming to their doorstep and pretend they are not at home until he leaves. As a result there are mounting number of family disputes and cases of domestic violence in the area. Even though their spouses agree to the idea of obtaining micro finance loans, they leave it to the women to settle payments as well. With no support from spouses and with mounting social pressure, women find it a challenge to carry the burden and opt to take their lives.

Borrowers turn debtors

Brick-making has evolved into a cottage industry and is one of the main sources of income for people in Maha Rathmale. But due to the prevailing rains, COVID-19 pandemic and Human-Elephant conflict the industry is facing a downward turn. T. M Kusumkumari makes a living from the brick industry. And as a last option to make ends meet she has obtained a micro finance loan. “It has been three years since I obtained a loan and have to settle Rs. 50,000. But they say I have to pay Rs. 69,000 with interest. We are a group of three women who applied for this loan. They asked us to sign a piece of paper, but there was nothing written on it. Subsequently they asked us to pay the interests. They have warned that they would take legal action if we don’t repay on time. We were given a card to mark how much we have paid and how much is remaining. But some of these cards were taken back as well,” complained Kusumkumari.

When we couldn’t pay off the debts the companies sent us letters. Then eight dealers representing the companies came home and threatened us

S. Madhuka Kumari with her three children

No mercy on us

One of the most unfortunate incidents was when one of the beneficiaries set herself on fire to escape social issues and the debt burden. We met S. Madhuka Kumari, a mother of five, currently recovering from the burns, but complains of aches and pains once in a while. She too was engaged in brick making and doing coolie work. Out of the five children two sons have been ordained as raising five children itself is a challenge. “My husband didn’t like the idea, but we didn’t have any option. I obtained a loan of Rs 135,000 and repaid Rs. 35,000. In the second instance I took Rs. 85,000 when I was expecting my youngest child. But I couldn’t repay the loan. When we couldn’t pay off the debts the companies sent us letters. Then eight dealers representing the companies came home and threatened us. I had a lot of fights with my husband and I set myself on fire while I was expecting my youngest child.” she recalled.

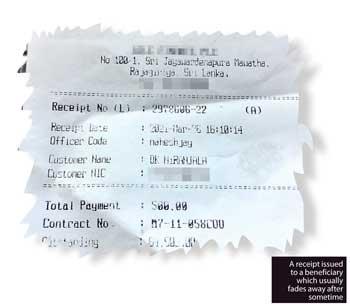

Most beneficiaries complain that they are now given a receipt instead of a card every time they pay off some amount, but the ink on the receipt fades away within a week. In most instances interests have accumulated and even though people have settled the amount they have obtained they continue to pay the interests. Therefore if someone has obtained Rs. 50,000 she has paid around Rs. 150,000 along with interests. “Dealers would come and stay at our houses until we give them at least Rs. 1000. Therefore there are many family disputes as well. They show no mercy on us,” Madhuka said with hopes that she would be able to get some relief in the future.

Intermediaries have escaped with money

Another issue is that most ‘deals’ are handled by intermediaries in respective villages. Therefore they would obtain installments from the beneficiaries and pay to the dealers. But one problem is that most of these intermediaries have escaped with the money. In one instance one of them escaped with 60 lakhs! This is an added burden to beneficiaries who have to keep on obtaining more loans to pay off their debts. K. H. N Wijerathne too has faced a similar plight. “I have to pay Rs. 32,000, but the company says I have to pay more with the accumulated interests. I took Rs. 120,000, but have paid thrice that amount with interests. All the cards were taken by the group leader, but now she’s not even in the village,” she complained.

When dealers visit them they give whatever money they have in hand just to rid themselves of the nuisance. But the money given that way isn’t recorded anywhere and most beneficiaries don’t have proof to show how much they have settled. Matters however don’t end there. The contracts and agreements they have to sign are printed only in the English language and beneficiaries complain that they have been asked to sign various papers. Sometimes their signatures are obtained on blank papers and subsequently forged on documents that beneficiaries have no clue about. Therefore nobody knows that’s there in a contract and they aren’t given any brief either.

It’s a trap, but now

it’s too late

In order to escape the debt trap beneficiaries tend to obtain multiple loans from various companies and even from money lenders. When they cannot pay off the debts they end up mortgaging jewelry and lands they own. J. P Kusumawathi sells carpets for a living. When we visited her house she was drying leftover cloth pieces to be patched to make carpets. But she hardly makes any profit. “It’s been a long time since I obtained these loans. At one point they said they would exempt us from the debts and we thought the matter was over. I paid installments continuously and then I faced many economic hardships and couldn’t settle the debts. I even sold a land. I have obtained loans from three places, but I have misplaced the cards because I have given it to various people to pay the money. Now they say they don’t have the cards with them. So I don’t know how much I have settled. We had no choice, but to get that money due to poverty. But once we realised that this was a trap it was too late,” she said, as tears welled up in her eyes.

I have obtained loans from three places, but I have misplaced the cards because I have given it to various people to pay the money. Now they say they don’t have the cards with them

J. P Kusumawathi makes a living from her carpet business

Weaknesses are an advantage

Many areas in Polonnaruwa are also gripped by the kidney crisis. Kidney patients are entitled to a Rs. 5000 relief allowance which they collect every month. But Microfinance dealers are smart enough to visit houses with kidney patients on the day they are supposed to collect their allowance. So without utilizing that money for dialysis purposes, they give the money to the dealers. M. B Chandra Kumari is one such kidney patient who has gone to the extent of mortgaging her land to pay off debts of the other two members in her team. “I have taken a loan of Rs. 130,000 and paid Rs. 77,000. But they say I have to pay Rs. 112,000 more. How could that be? They don’t have records of the amounts we have settled. So we have refused to pay until we know the exact amount. This is a manipulation to obtain more money and they’re exploiting our weaknesses,” said Chandra Kumari.

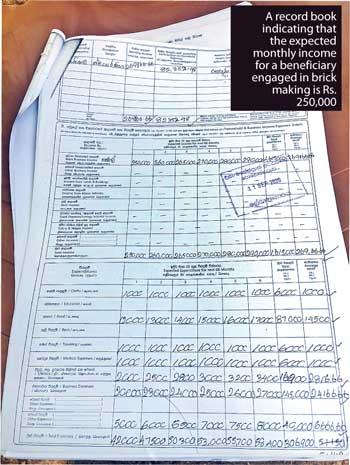

The Daily Mirror also observed how dealers representing micro finance companies have manipulated people. In one record book, a dealer has noted that a beneficiary’s primary source of income is brick making and the expected monthly income is Rs. 250,000!

In Welikanda, women have now taken up male-dominated professions

We then travelled to Welikanda and realised that the situation there is different to that of Maha Rathmale. Here, women have resorted to male-dominated professions such as sand mining, road constructions in their quest to earn an income and pay off debts. We met D. K Niranjala and Nirmali Lasanthika, two women who earn an income from their boutiques. “We have taken loans since 2010 and have been repaying. We started with 10,000 and the last amount was Rs. 90,000. But when they said they would exempt us from these debts we didn’t pay. However, they have added interests during the period we stopped paying. We don’t get loans from state banks. Some women find work in farms, one of them went to work at the Batticaloa Campus when it was converted to a quarantine Centre. These dealers come and scold us in filth. We earn an income from the boutiques and we hope that they may not go to courts. If that happens we have to pay Rs. 23,000 extra with lawyer’s charges, documentation fees etc. But some lawyers don’t even speak for their clients. They just take the money and don’t fight the case,” Niranjala and Lasanthika said in one voice.

These dealers come and scold us in filth. We earn an income from the boutiques and we hope that they may not go to courts

D. K Niranjala (left) and Nirmali Lasanthika from Welikanda

A massive fraud

The Central Bank of Sri Lanka states that as of March 30, 2020 there are only four institutions licensed to carry out micro finance activities. But with the end of the civil war around fifty established financial institutions including subsidiaries of major banks reportedly entered the micro finance business. Amongst them were a mushrooming number of unregulated micro finance companies. The existing legal loopholes and backlog of draft acts that never saw light of day have made it easier for mushrooming micro finance companies to do as they please.

Shedding light on the legal lacuna, Attorney-at-Law Radhika Gunaratne pointed out that a main problem is in the contracts given to beneficiaries. “According to the contract law both parties should read an agreement, but how can borrowers read them when they are in English? These companies charge exorbitant interest rates which are not even mentioned in the contracts. But how would borrowers know when they can hardly place a signature on the documents? Those who borrow money don’t have any financial literacy. All that they want is money and they aren’t aware of the consequences thereafter.”

Gunaratne has been doing pro-bono legal work for micro finance debtors, but there’s a limit to what she could do. “How can we fight individual cases when there are number of cases this way? Microfinance in Sri Lanka is a money-lending business. The Central Bank is the apex institution to regulate this process. We are now in the process of analysing how we can incorporate a criminal liability to these cases. Most women commit suicide due to harassment. They have to place collateral and this is usually a television set or a bike that is in their husband’s name. If not it is a person who appears as collateral.” said Gunaratne.

Even though the Microfinance Act No. 6 of 2016 was enacted in July 2016 it has been observed that the legislation doesn’t necessarily reduce ambiguity in the existing Microfinance environment. However, Gunaratne said that a new Bill titled the Credit Regulatory Authority Bill is likely to be introduced with the primary objective of regulating all moneylending businesses and micro finance institutions. “But companies registered under the Finance Business Act No. 42 of 2011 have been excluded from it,” she continued. However, with the permit issued by CBSL these companies can do micro finance activities or money-lending. But this contradicts the micro finance concept. “Around 30 cases have been filed so far but the accused party withdrew the cases during pre-trial stage as they were guilty of many actions. For instance, they forge signatures. Once a beneficiary places her signature on a piece of paper, the companies would scan it and place the signature when agreements are being renewed. Sometimes people are asked to pay more than they expected but they are trapped because they are being told that they have signed the documents. Many aren’t even aware of signing such a document but they don’t have evidence to fight such injustices.

“These companies are also in the habit of bribing lawyers appearing for victims. So they don’t fight the case. Most companies claim interests of over 200%. This is a massive fraud,” she said while adding that most companies are trying to portray themselves as the most successful in the micro finance business.

Minister not available

Several attempts to contact State Minister of Microfinance and Self-Employment Shehan

Semasinghe proved futile.

Successive govt.s responsible for prevailing situ

As mentioned before, many borrowers complain that they weren’t informed about interest rates. But Lanka Microfinance Practitioners Institution President Anura Atapattu holds a different view. “People can say all these things. But there are two ways in which interests are charged; one is the flat rate and the other is the declining rate. If a loan of Rs. 10,000 has been obtained at an interest rate of 10% then Rs. 1000 is the interest. If that is paid monthly then the loan amount reduces. So during the second month the borrower has to pay Rs. 9000 and it continues. This is called the flat rate and is calculated at the beginning. On the other hand, the declining rate is calculated at the time of repaying debts. The lender calculates the interest for the period during which the loan has been obtained. The relationship between flat rate and declining rate is as follows – flat rate x 2 – 2 = declining rate. For example 10% x 2 = 20% - 2 = 18% therefore 10% of flat rate is equal to 18% declining rate.

“But now the CBSL has introduced an interest cap of 35%. But in this scenario people think 10% flat rate is a better deal than the 18% declining rate. Some even go for a 15% flat rate. People are also charged a documentation fee and if they delay to pay they are charged with a penalty.

“People need to be careful when they obtain loans and they should clear any doubts,” Atapattu further opined in response to a query on claims that lenders never educate borrowers about interest rates. “Microfinance was initially handled by non-governmental organisations and then the government took over. But to date there is no regulatory framework. Prior to 2016 there were around six draft Acts that were never approved by consecutive governments. Some have even reached Parliamentary Committee level but that was that. Without a proper act how can there be a regulation on micro finance companies. Successive governments are responsible for the prevailing situation. It has affected a large number of people while an equally large number of people are gaining profits from this business.” said Atapattu.

28 Dec 2024 2 hours ago

28 Dec 2024 2 hours ago

28 Dec 2024 3 hours ago

28 Dec 2024 3 hours ago