In the last 70 years, Sri Lanka has never been in a more precarious position with regard to the repayment of its debt, than at present, in December 2021. There is much that is said in the media about the increase in Sri Lanka’s debt and as is the case with any crisis, there is a great deal of political finger pointing with regard to the causes of this debt increase.

In the last 70 years, Sri Lanka has never been in a more precarious position with regard to the repayment of its debt, than at present, in December 2021. There is much that is said in the media about the increase in Sri Lanka’s debt and as is the case with any crisis, there is a great deal of political finger pointing with regard to the causes of this debt increase.

How did the debt increase so much, especially in the last five years and who or what is responsible for the increase in Sri Lanka’s debt? This insight is a studied response to that question.

Increase in Sri Lanka’s debt 2015-2019

The comprehensive analysis set out here shows that the main driver of the increase in Sri Lanka’s debt over the years is the interest that needs to be paid on past debt. The analysis also provides a precise estimation of how much past debt has contributed to the increase in debt from 2015-2019.

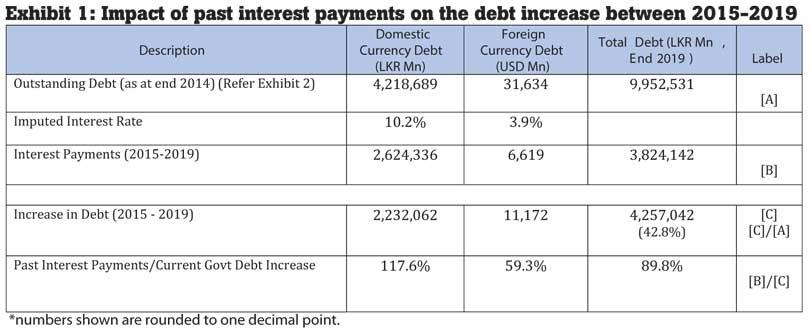

The analysis finds that Sri Lanka’s total debt stock increased by 42.8 percent during 2015-2019 and at least 89.8 percent of that increase was due to the interest cost on accumulated past debt. Exhibit 1 sets out the highlights of the calculation and its parameters.

Deconstructing calculation

One reason that there is much confusion about the calculation is because estimating the increase in debt and finding the sources of debt increase is complicated by a few factors. The present analysis explains and navigates four sources of complications in calculating the changes to Sri Lanka’s debt.

(1) Interest cost estimation: Estimating the cost of interest is non-trivial due to the manner in which data is available and the need to separate out the interest costs on new debt, from the interest cost of previously accumulated debt.

(2) Arbitrary accounting: Central government debt is sometimes arbitrarily moved back and forth, out of the books of the central government and not consistently reflected in debt reporting, despite it being a continued debt obligation of the central government.

(3) SOE guaranteed debt: There is debt in the books of state-owned enterprises (SOEs), which the central government is explicitly responsible for, because it is supported by sovereign guarantees or letters of comfort issued by the central government.

(4) Foreign currency debt: Debt is taken and repaid in local currency as well as foreign currency. The method used to calculate debt increase in a single currency is often flawed. When the method is correct, calculations of the percentage increases in debt give the same result irrespective of the currency in which the debt is counted.

(5) Active liability management: This is a legal provision under which the government can raise debt to settle future debt, rather than present debt and is then required to carry the borrowed funds as a cash asset in a designated account. This is an effective increase in debt only when that cash asset is utilised.

Interest cost estimation

How was the interest cost estimated? Two valid methods were tested for this estimation for both domestic and foreign currency debt. They yielded proximate results. But the final estimations used in this insight drew on whichever method that gave a lower interest cost – therefore the estimations are conservative.

Domestic currency debt: The interest quantum of the domestic currency debt was calculated by adding up the yearly interest payments reported by the Central Bank of Sri Lanka and adjusting it downwards by subtracting the estimated interest payments on additional debt taken (beyond what was needed to pay interest on past debt) from 2015-2019.

Therefore, the effective interest rate for the period is an imputed figure based on the quantum of interest that was actually paid, adjusted downward to reflect only the interest cost attributable to past debt.

SOE debt, because it is perceived as more risky, is generally secured at a higher interest rate than central government debt. However, since precise information on the interest rate on SOE debt was not available, we made the assumption that SOE debt was serviced at this same effective interest rate that was imputed for central government debt. Therefore, it is a conservative estimation that could slightly understate the total interest paid on SOE debt.

Foreign currency debt: The Central Bank reports the average interest rate by debt instruments. The weighted average interest rate of the foreign currency debt for the period 2015-2019 was calculated based on the quantum of debt within each instrument. Applying the more detailed methodology used to calculate domestic currency interest rate resulted in a higher imputed interest rate on foreign currency of 4.2 percent. Therefore, the 3.9 percent rate used is also a conservative calculation that is likely to under-estimate the total interest on foreign currency debt. Applying the 4.2 percent rate results in the cost of interest on accumulated debt rising from 89.8 percent to 92.4 percent of the debt increase during 2015-2019.

Arbitrary accounting

A certain amount of central government debt is sometimes arbitrarily moved back and forth, out of the books of the central government in different years. This problem has been carefully studied and set out in a previous insight by Verité Research, titled: Navigating Sri Lanka’s Debt – Better Reporting Can Help. Two examples of such movements in the central government debt, can serve to demonstrate the problem.

(1) US $ 828 million in central government debt, taken from the Exim Bank of China for the Puttalam Coal Power Plant was transferred from the books of the central government to the books of the Ceylon Electricity Board in 2014 and subtracted from the reporting of the central government debt in that year. This served to show a significant decrease in the total government debt in 2014, through an accounting sleight of hand.

(2) US $ 951 million in central government debt, taken from the Exim Bank of China for the Hambantota Port Development Project was transferred from the books of the central government to the books of the Sri Lanka Ports Authority in 2014 and subtracted from the reporting of the central government debt in that year. The National Audit Office (NAO) notes that in 2017, the Hambantota Port Development debt was transferred out of the books of SOEs and not properly recognised within the central government debt either. If such movements are not followed and properly factored into the substantive analysis, it would result in misunderstanding the changes in central government debt.

SOE guaranteed debt

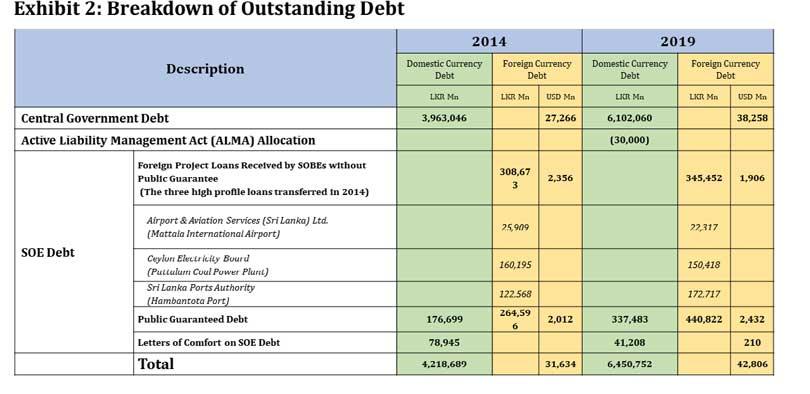

A breakdown of the external debt owed by the central government is published by the Central Bank of Sri Lanka. However, this is only a subset of the total debt for which the government is liable. Accounting for the additional debt is made onerous by the fact that the financial reporting of the government does not provide ready visibility of the composition of external public debt by indebted institution.

The central government is indirectly liable for the debt of SOEs. However, it is directly liable for that debt when it provides guarantees or letters of comfort to the lender, for debt taken by SOEs. In calculating the changes to central government debt over time, it is therefore necessary to account for at least the SOE debt that is under guarantees or letters of comfort by the central government.

Exhibit 2 provides an analysis of the SOE debt that is under the direct obligation of the central government, between 2014 to 2019.

Foreign currency debt

Calculations on debt increase that are discussed in public tend to engage in the summation of LKR and USD-denominated debt, using an incorrect method. It is incorrect because the result of the summation is sensitive to the currency in which it is done. It would result in over-stating the increase in debt if it was summed up in LKR and would be under-stating the increase if it was summed up in USD.

The error is created by using different exchange rates for the currency conversions of the debt stocks held in different years. The consequence of this error is that if the total debt is reported in LKR, it misrepresents the consequence of LKR currency depreciation as if it were an increase in borrowing – whereas it is not actually an increase in borrowing but simply an increase in the LKR value of past USD-denominated borrowing. Likewise, if the total debt is reported in USD, this error has the consequence of making the results of currency depreciation appear as if it were a decrease in borrowing – whereas it is not actually a decrease in borrowing but simply a decrease in the value of past LKR-denominated borrowing, when converted to USD terms.

The error is avoided by applying a single exchange rate to convert the debt stocks being compared and stated in a single currency. That way, the calculation of debt increase is independent of the currency in which that calculation is made.

Active liability management

Active Liability Management Act No. 8 of 2018 was a new structure introduced by the government to allow the government to proactively smoothen its borrowing and reduce the lumpy refinancing and roll-overs of its debt. The Active Liability Management Act (ALMA) was approved by Parliament in March 2018. It allows the government to borrow ahead of time to finance future debt repayments.

The debt raised under the ALMA cannot be utilised by the government for its expenditures. Under the ALMA, it is required that the principal and the interest, if any, is maintained in a designated account and remains an asset of Sri Lanka under the Consolidated Fund and be ring-fenced such that the money can only be used for the purposes of refinancing and pre-financing. That is, borrowings kept under the ALMA are effectively not an increase in the government’s net-liabilities, as the liability created by the borrowing is offset by a cash asset held in the designated ALMA account.

A resolution was passed by Parliament in July 2019 to raise up to Rs.480 billion under the ALMA. However, the financial reporting by the Finance Ministry makes it possible to trace only Rs.30 billion as having been formerly placed within the framework and recognised within the borrowing of 2020, instead of 2019. Therefore, the ALMA transaction in 2019 hardly has an impact on the calculation of debt increase but for the purpose of accuracy, it is required to be included in the methodology of calculating the changes in debt over time and is therefore included in the present calculation.

(Verité Research is an independent think tank based in Colombo that provides strategic analysis to high level decision makers in economics, law, politics and media. Comments are welcome. Email [email protected])